(Mike Maharrey, Money Metals News Service) Are we in the early stages of a fundamental shift in global monetary history?

Analysts at Deutsche Bank Research Institute think we are. They see a future where the dollar plays a much smaller role.

As the USSR’s empire crumbled, Francis Fukuyama proclaimed that humanity had reached “the end of history.” The U.S. was the unchallenged global hegemon with unprecedented military and economic power. Central banks sold gold and accumulated dollars.

Things have changed in recent years, and there has been an undeniable de-dollarization trend.

Even before Russia invaded Ukraine, many central banks were accumulating gold. With the U.S. weaponization of the dollar after the Russian invasion, the pace accelerated.

In a detailed research report, Deutsche Bank analysts Mallika Sachdeva and Michael Hsueh argue that “the end of history has come to an end.”

“The world is back in a superpower struggle; the U.S. is retreating from free trade, alliances, and security provision; the Great Economic Moderation is behind us; and the dollar banking system has been weaponized. The ‘return of history’ has big implications for gold and the dollar.”

Is De-Dollarization Real?

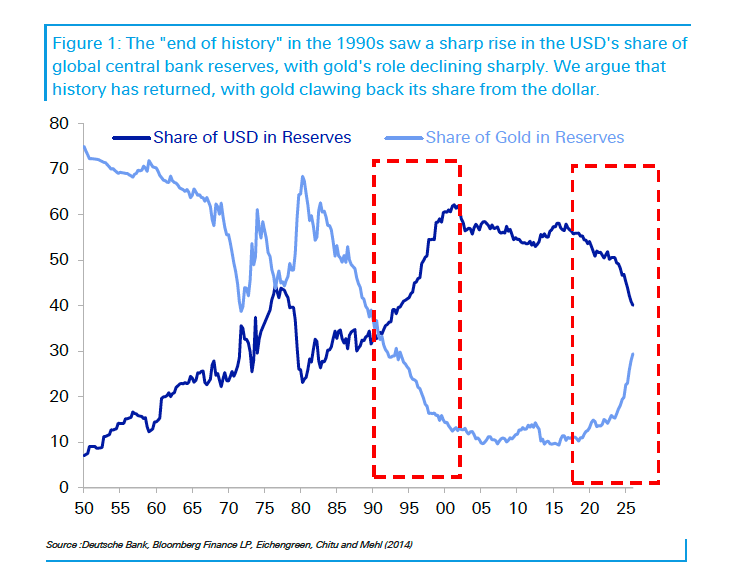

Some people claim the de-dollarization trend his overhyped, but the data is hard to ignore. The share of dollars in global central bank reserves has dropped sharply from around 60 percent to around 40 percent today. Meanwhile, the share of gold has doubled in the last four years to around 30 percent.

“Before the 1990s, gold had consistently been a larger share of central bank reserves than the fiat dollar. But by the end of the 1990s, the dollar was over four times the share of gold. This seems to now be going in reverse, with gold clawing back its share rapidly. What happened in the 1990s and why is this unwinding today? How far can it go and to what end?”

De-dollarization skeptics counter that the rapid rise in the share of gold reserves is purely a function of rising prices. But Sachdeva and Hsueh argue that the rise in gold price is at least partly a function of central bank gold buying.

“There is a genuine volume driver underlying this: central bank purchases have arguably themselves been behind significant price momentum. There is indeed a close relationship between official purchases and sales of gold and the change in the real gold price. Volume and prices are thus endogenously related and are both doing the legwork of gold’s rising share.”

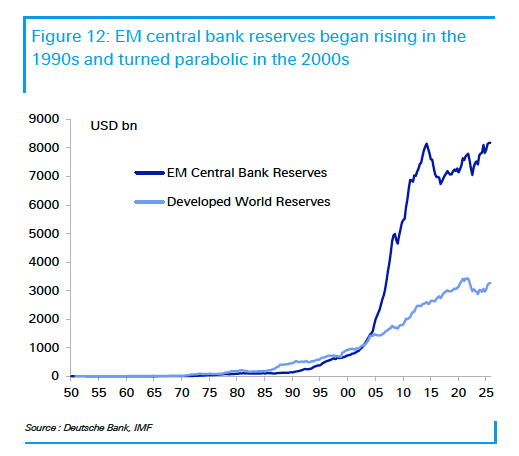

Virtually all the central bank gold buying has come from emerging markets. Since 2008, emerging market central banks have gobbled up 225 million ounces of gold. Sachdeva and Hsueh expect the trend to continue, noting that even with the recent pace of purchases, EM central banks still hold half the amount of gold as developed market banks.

The End of History

Sachdeva and Hsueh believe that the decline of gold and the rise of the dollar weren’t solely due to the end of Bretton Woods. They think it was driven more by geopolitical shifts.

“It was not a transition in the monetary system – which had occurred two decades prior – but a shift in the geopolitical environment that changed the role of gold.”

With the USSR gone, the U.S. was not only the biggest kid on the block; it was virtually the only kid in the neighborhood with any muscle at all.

“The U.S. thus became an uncontested hegemon in what appeared to be a geopolitically unipolar world. Japan, which had been the U.S.’s closest economic competitor, was well within the US security and dollar system, and China was still a decade from joining the WTO.”

In this environment, everybody wanted dollars. EM central bank dollar reserves went parabolic around 2000.

“In sum, the biggest driver of gold’s decline in global reserves in the 1990s was the rise of EM FX reserves accumulated in USD. This was in turn a function of dramatic globalization, in a US-driven neo-liberal unipolar order, amidst sound and improving economic fundamentals in the U.S.”

De-Dollarization Ramifications

Things have changed. Many countries are now wary of holding dollars. They don’t want to be subject to U.S. foreign policy bullying, and they are concerned about America’s fiscal malfeasance. The 2008 financial crisis was a canary in a coal mine. Aggressive sanctioning of Russia after it invaded Ukraine may have been the final straw.

Sachdeva and Hsueh point out several trend reversals from the 90s that seem to be driving de-dollarization.

- The U.S. is stepping back from free trade and fracturing traditional alliances.

- The relationship between the U.S. and emerging markets is reversing. In the past, the U.S. outsourced manufacturing while EM countries outsourced security and savings. Today, the U.S. is onshoring more critical manufacturing, while many EM regions like Asia and the Gulf will be reconsidering their need for strategic autonomy in areas like energy and defense.

- The U.S. has lost control of its inflation dragon.

- The weaponization of the dollar.

“The end of history has itself come to an end, with significant implications for gold and the dollar, which are becoming increasingly apparent.”

This is a fancy way of saying that if de-dollarization and EM gold accumulation continue, it could drive the gold price even higher. According to Sachdeva and Hsueh, for every 1 million ounces of gold purchased by central banks, the price rises by 1 percent.

Sachdeva and Hsueh ran four different scenarios with varying levels of de-dollarization and central bank gold buying. They determined that “even in an environment where EM FX reserves decline to $5 trillion, gold prices could still rise to $8,000 over the next five years, if EM countries all target a 40 percent gold share.”

It could also signal a fundamental shift in the global monetary order.

“In sum, while EM central bank diversification into gold likely has much to do with preserving the value and accessibility of their foreign savings in a changing geopolitical climate, it may also – in the long run – play a role in anchoring a monetary order that builds independence from the dollar. There is, of course, a very long way to go. EM central banks as a whole still only hold half the physical gold of advanced economy central banks. But there is a world where gold returns to the center of a future monetary system with different leaders.”

As I’ve mentioned over and over, even a modest de-dollarization spells big trouble for the U.S. economy.

Since the global financial system runs on dollars, the world needs a lot of them, and the United States depends on this global demand to underpin its bloated government. The only reason the U.S. can borrow, spend, and run massive budget deficits to the extent that it does is the dollar’s role as the world reserve currency. It creates a built-in global demand for dollars and dollar-denominated assets. This absorbs the Federal Reserve’s money creation and helps maintain dollar strength despite the Federal Reserve’s inflationary policies.

But what happens if that demand drops? What happens if BRICS nations and other countries don’t need as many dollars?

A de-dollarization of the world economy would cause a dollar glut. The value of the U.S. currency would further depreciate. At the extreme, global de-dollarization could spark a currency crisis. You and I would feel the impact through more price inflation, eating away at the purchasing power of the dollar. In the worst-case scenario, it could lead to hyperinflation.

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

{kind=link}