(Mike Maharrey, Money Metals News Service) No matter how you slice the data, it keeps coming up inflation.

The April CPI data did nothing to allay fears of renewed inflationary pressure as rising energy prices continued to impact the economy.

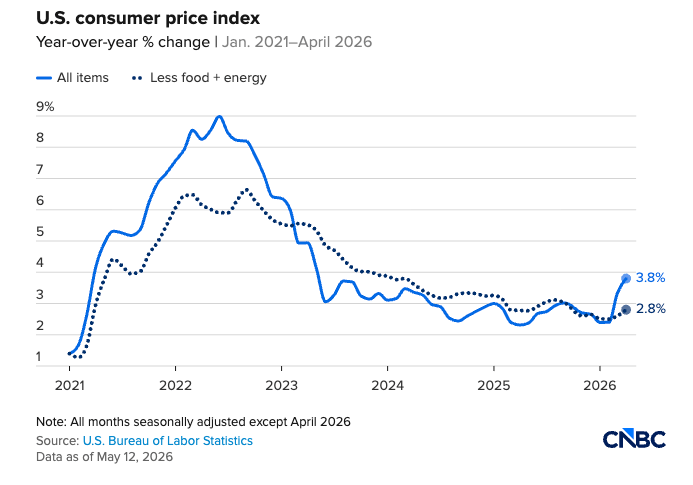

On a monthly basis, the CPI rose 0.6 percent, adding to the 0.9 percent rise in prices in March. That drove the annual CPI to 3.8 percent, the highest level since May 2023.

The monthly increase was as forecast, with the annual CPI coming in just above expectations.

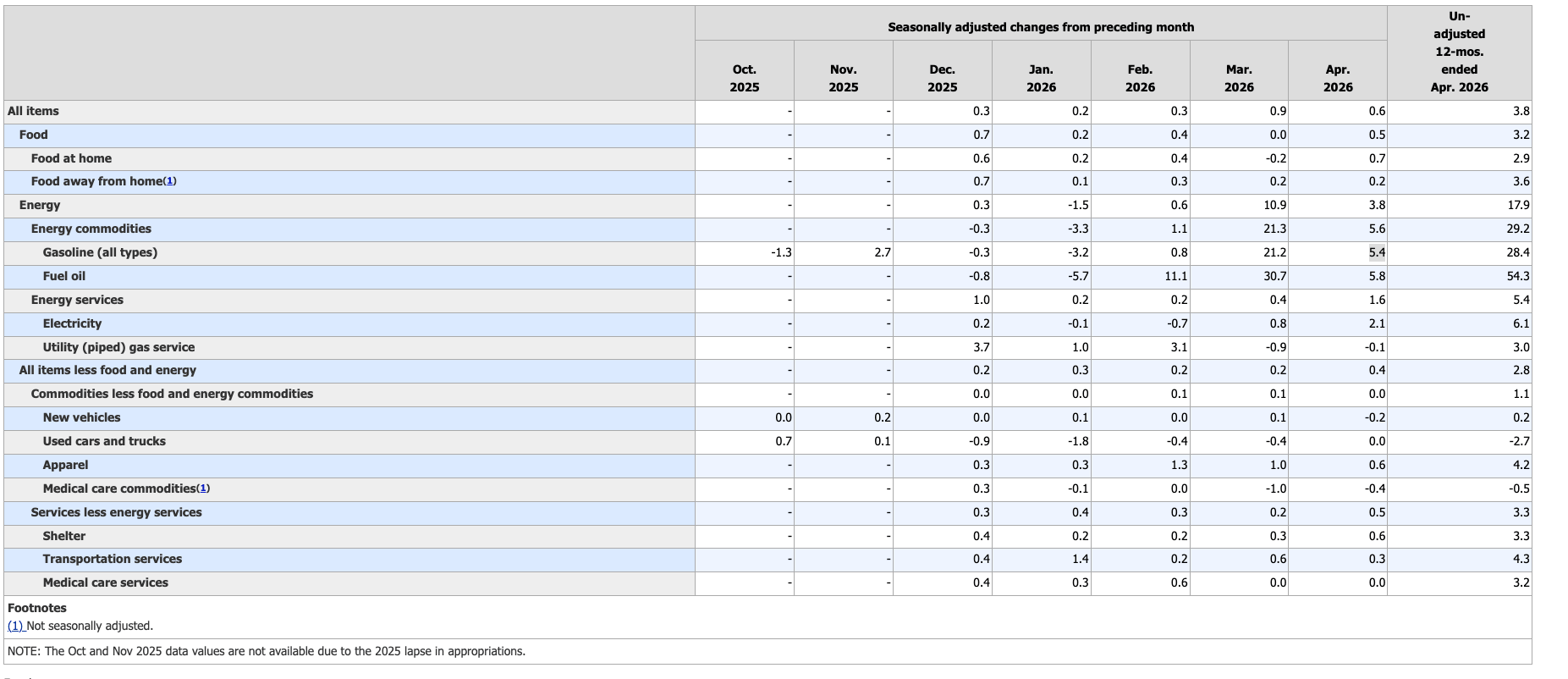

Unsurprisingly, spiking energy costs as the Iran war drags on had a significant impact on the overall CPI, contributing about 40 percent to the overall jump. The energy index rose 3.8 percent last month, driven by a 5.4 percent increase in gasoline prices. Gasoline is up 28.4 percent from one year ago.

More concerning is that we’re starting to see prices tick up in other categories. Core CPI, stripping out more volatile food and energy costs, rose 0.4 percent in April, pushing annual core CPI to 2.8 percent.

It’s important to point out that core CPI remains above the Fed’s stated 2 percent target and has been mired in this range for well over a year. This indicates that recent price inflation isn’t merely reflecting an oil shock. There is underlying inflationary pressure in the system (more on that in a moment).

Breaking down the data, we find food prices rose 0.5 percent in April, and the shelter index spiked by 0.6 percent. Service price (less energy services) also rose 0.5 percent.

As I mentioned, any time I report on government CPI data, it’s important to take this (and every) CPI report with a grain of salt. It is still factoring in November data that they basically just made up. And the constant revisions to the labor data should also make you skeptical of government numbers.

You also need to remember that the CPI data understates price inflation by design. The government revised the CPI formula in the 1990s so that it understated the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers. So, if the BLS used the old formula, we’d be looking at CPI closer to 6 percent. And using an honest formula, it would probably be worse than that.

However, this government data drives decision-making, so we need to pay attention to what it tells us.

The Underlying Inflation Story

The CPI doesn’t tell the full inflation story. It simply reflects the price movements of a basket of goods made up out of thin air by the number crunchers at the BLS. Yes, this does give some indication of the trajectory of price inflation. However, it tells us little to nothing about the inflation trajectory as economists have historically defined it.

Inflation is not “rising prices.” Increasing consumer prices are one symptom of inflation, defined as an increase in the supply of money and credit. Rising consumer prices are a symptom of this monetary inflation.

Other factors – such as oil shocks – also raise a lot of prices. We see that in the current CPI data. However, this is fundamentally different from monetary inflation, which is only caused by one thing – government/central bank money creation.

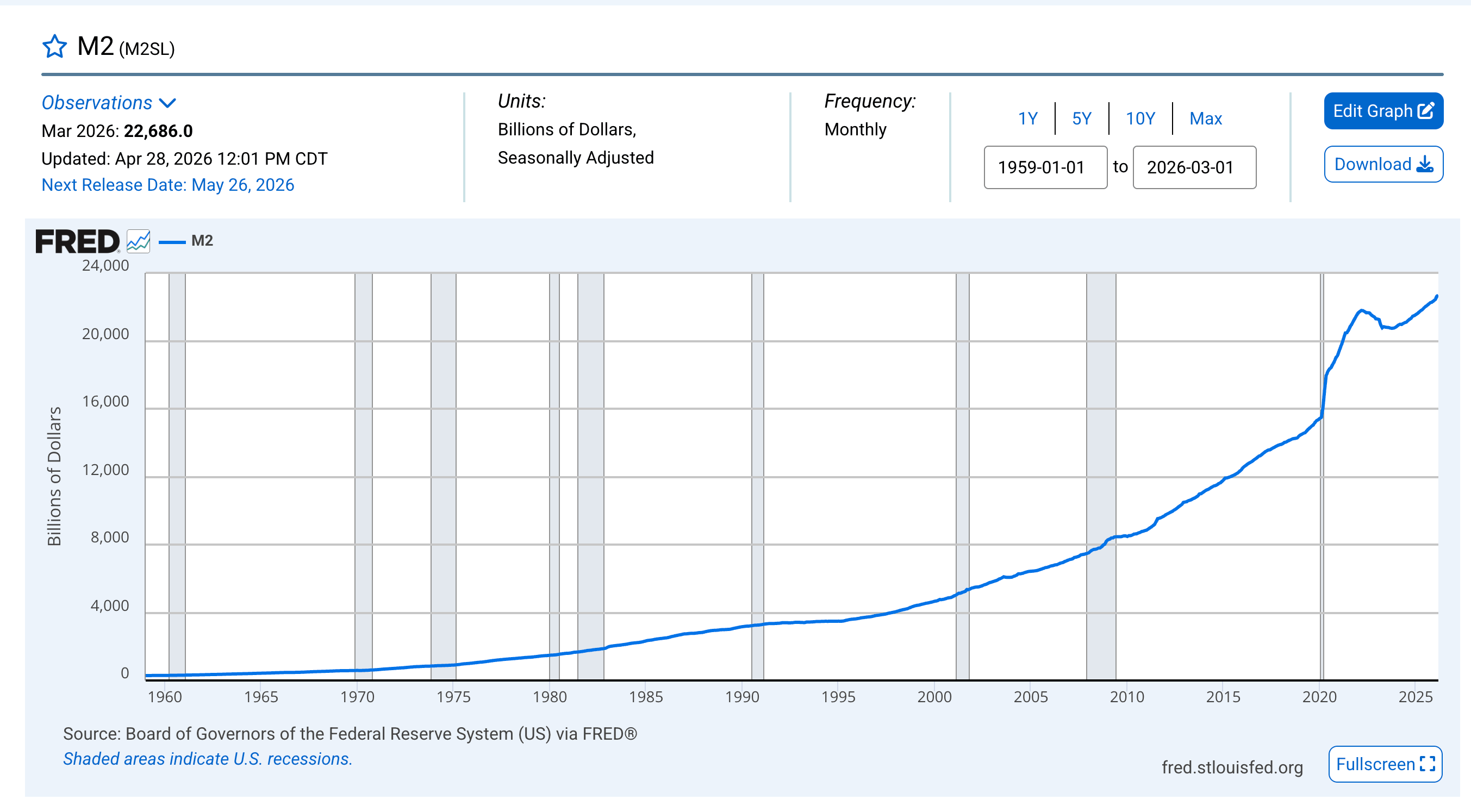

And if we look at the money supply, we find that inflation (properly defined) is heating up, with or without an oil shock.

In fact, if we use the economic definition of inflation as an increase in the money supply, the inflation rate is much higher – double the CPI.

Based on the Fed’s M2 data, the money supply increased from $21.61 trillion in February 2025 to $22.67 trillion in February 2026, a 4.9 percent increase.

In other words, we have an actual inflation rate of nearly 5 percent.

The M2 money supply increased by another $57 billion in March.

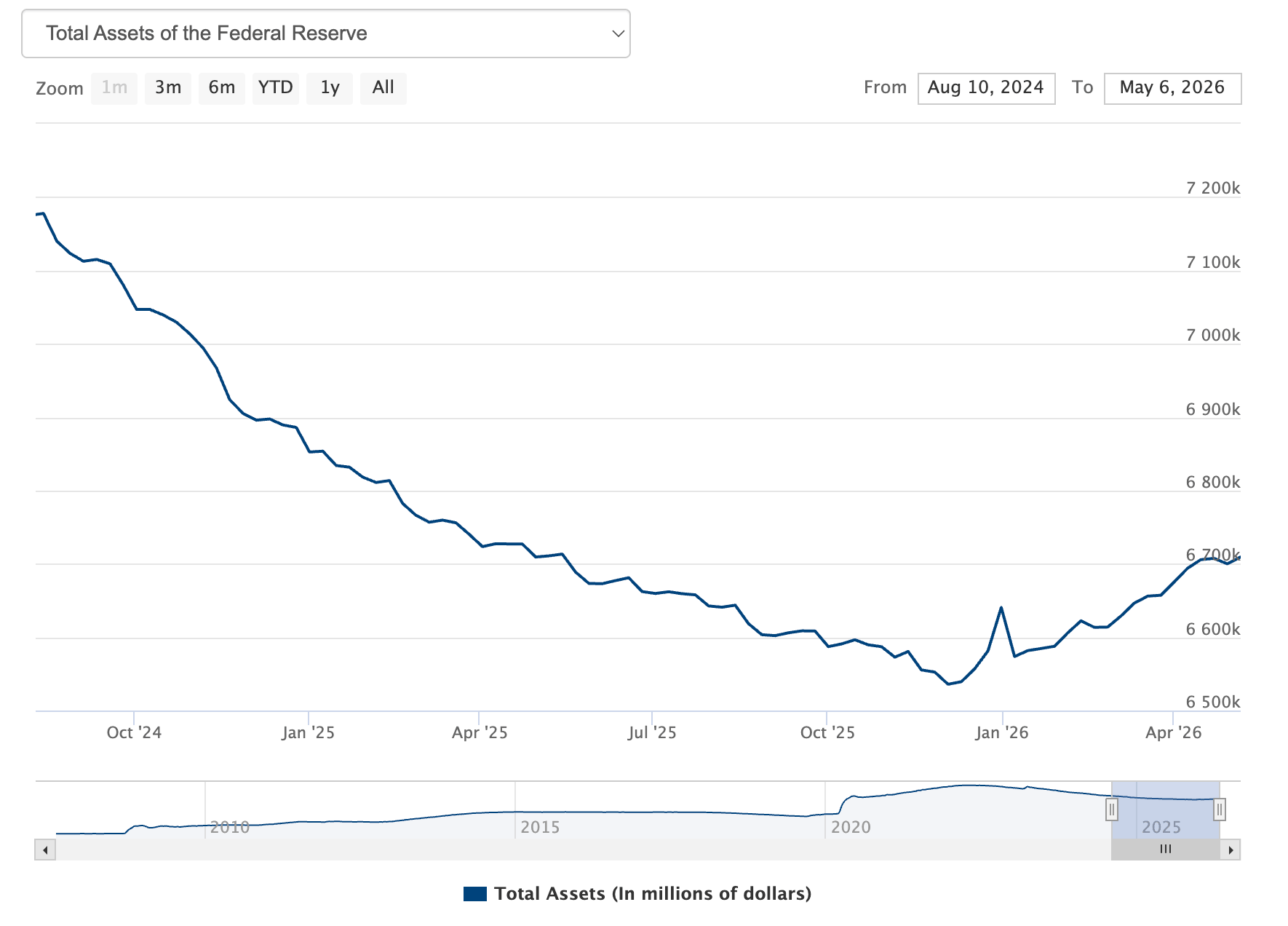

We also know inflationary pressures are increasing because the Federal Reserve is once again expanding its balance sheet.

While you’ll never hear anybody at the Fed utter the term, the central bank relaunched quantitative easing in December. That means they are once again buying U.S. Treasuries using money created out of thin air.

Ultimately, this monetary inflation will work its way through the economy. It will either manifest in rising asset prices or rising consumer prices. Ultimately, it is devaluing your money (by design).

If the U.S. and Iran can negotiate a permanent end to hostilities, this oil shock will quickly pass. The pundits and prognosticators will claim the inflation problem is gone. It won’t be. As long as the government keeps creating money, the inflation problem will persist.

Plan accordingly.

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

{kind=link}