(Mike Maharrey, Money Metals News Service) Based on the CPI, inflation is relatively cool. Don’t be fooled. It’s much higher than advertised, and you can see it clearly if you look at the right data.

When talking heads on CNBC or Fox Business talk about inflation, they always reference the Consumer Price Index (CPI). This metric measures the price changes in a “basket of goods.” This gives a fair approximation of price inflation (although intentionally understated), but it doesn’t give us a good gauge on the trajectory of inflation as historically economically defined.

Inflation isn’t just “rising prices.” Historically, inflation was defined as an increase in the quantity of money and credit. In other words, inflation (properly defined) isn’t caused by “oil price shocks” or greedy corporations hiking prices. It is caused by money printing.

A generally rising price level is one symptom of this monetary inflation. This will be reflected by the CPI. However, rising consumer prices aren’t the only manifestation of this phenomenon. Monetary inflation also drives asset price inflation. Much of the stock market gain in recent years was due to inflation. This is also one of the reasons the price of gold keeps climbing.

The point is that it’s very important to distinguish between price inflation and monetary inflation. Mainstream financial pundits and many economists fail to do so, and it creates a great deal of confusion.

What Is the Real Inflation Rate?

Based on the CPI, the annual inflation rate is currently 2.4 percent. Pundits call this the “inflation rate,” but it really only tells us that the price of this government-created basket of goods has gone up 2.4 percent in the last 12 months.

This is viewed as only a slightly elevated “inflation rate,” given the 2 percent goal. (Never forget that it is the stated policy to devalue your purchasing power by 2 percent every year.)

However, if we use the economic definition of inflation as an increase in the money supply, the inflation rate is much higher – double the CPI.

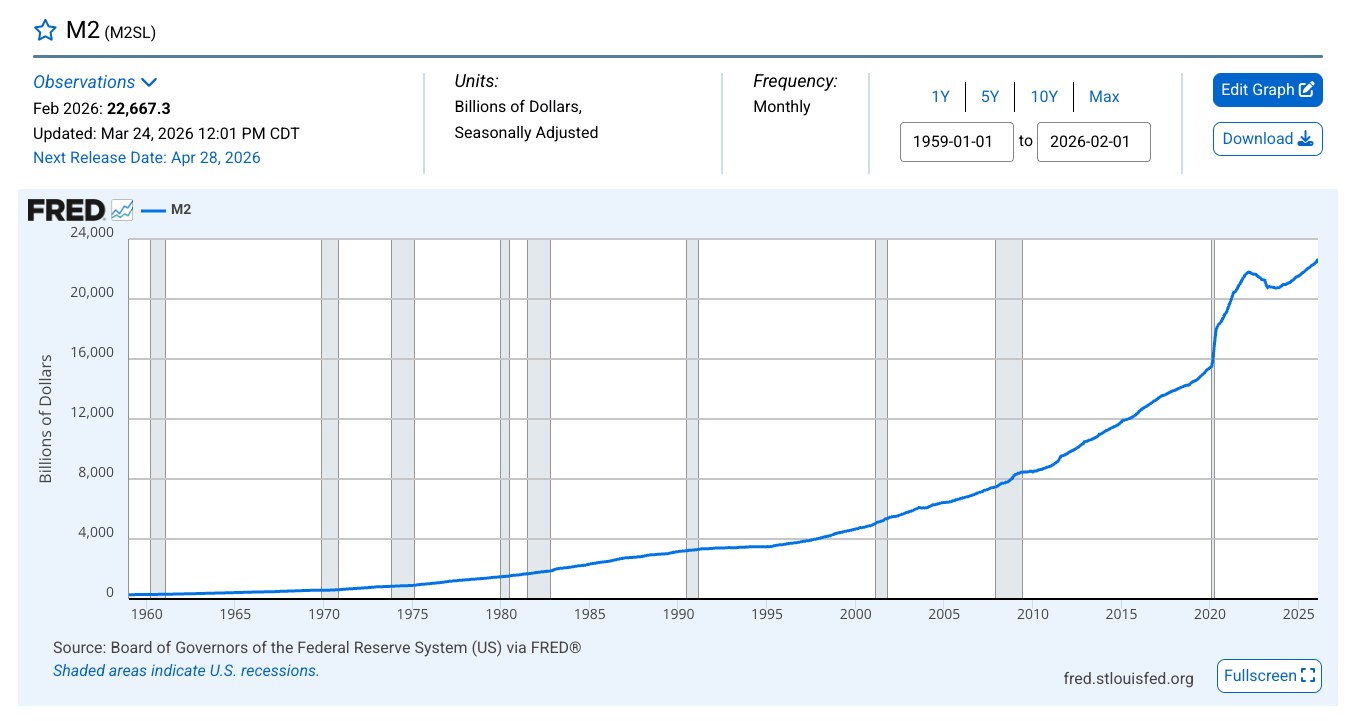

Based on the Fed’s M2 data, the money supply has increased from $21.61 trillion in February 2025 to 22.67 trillion in February 2026.

That represents a 4.9 percent increase.

In other words, we have an actual inflation rate of nearly 5 percent.

Inflation Is Heating Up

Based on the trajectory of the money supply, inflationary pressure is increasing, not abating (oil prices notwithstanding).

After peaking in April 2022, the money supply began to decline as the Fed hiked rates that year. The money supply bottomed in October 2023 and began increasing again. The money supply is now well above the pandemic peak.

And money creation has accelerated over the last several months. In fact, the money supply is growing at the fastest rate since July 2022, in the early stages of the tightening cycle.

This undercuts the notion that monetary policy is “tight.”

While it may be too tight for an economy dominated by a massive Debt Black Hole, it is not tight by historical standards, which is exactly why the money supply is increasing.

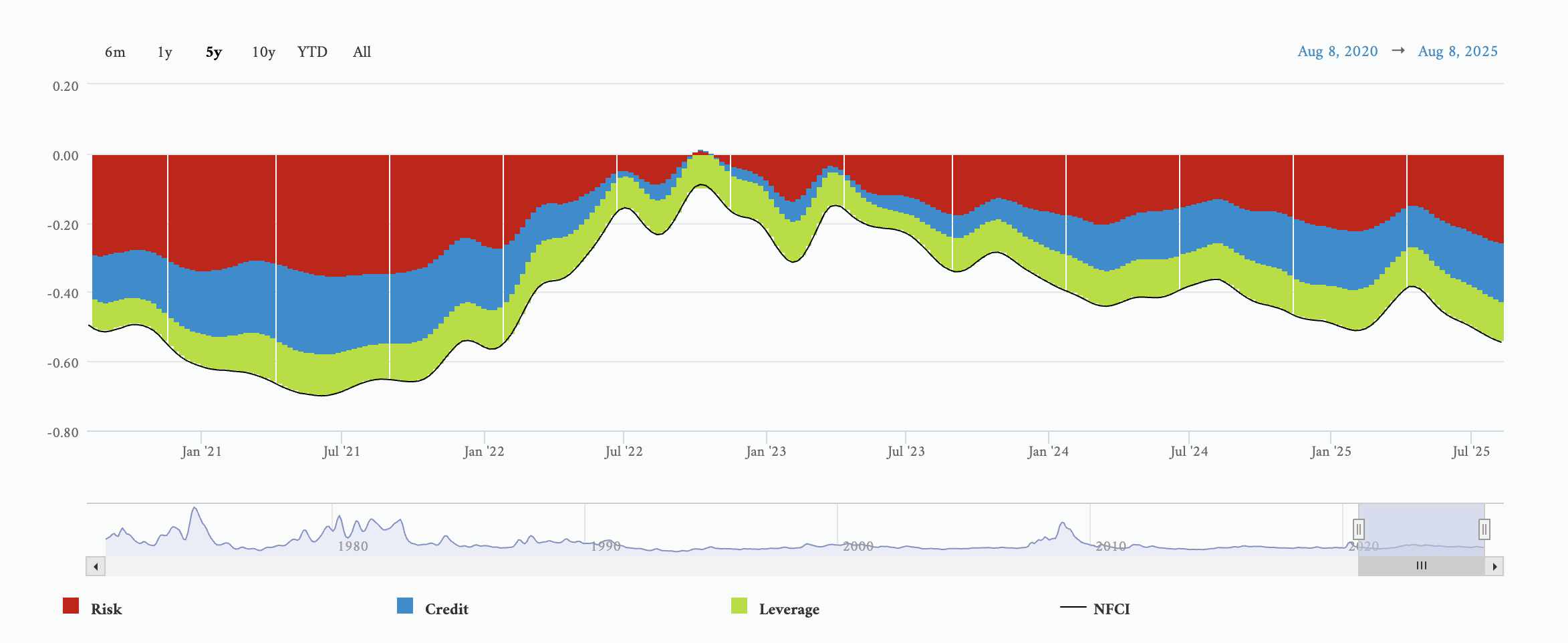

The Chicago Fed’s National Financial Conditions Index confirms this. As of the week ending March 20, the NFCI stood at -0.48. That negative number represents historically loose financial conditions.

Interestingly, the NFCI never went positive, even during the peak of the Fed’s tightening cycle.

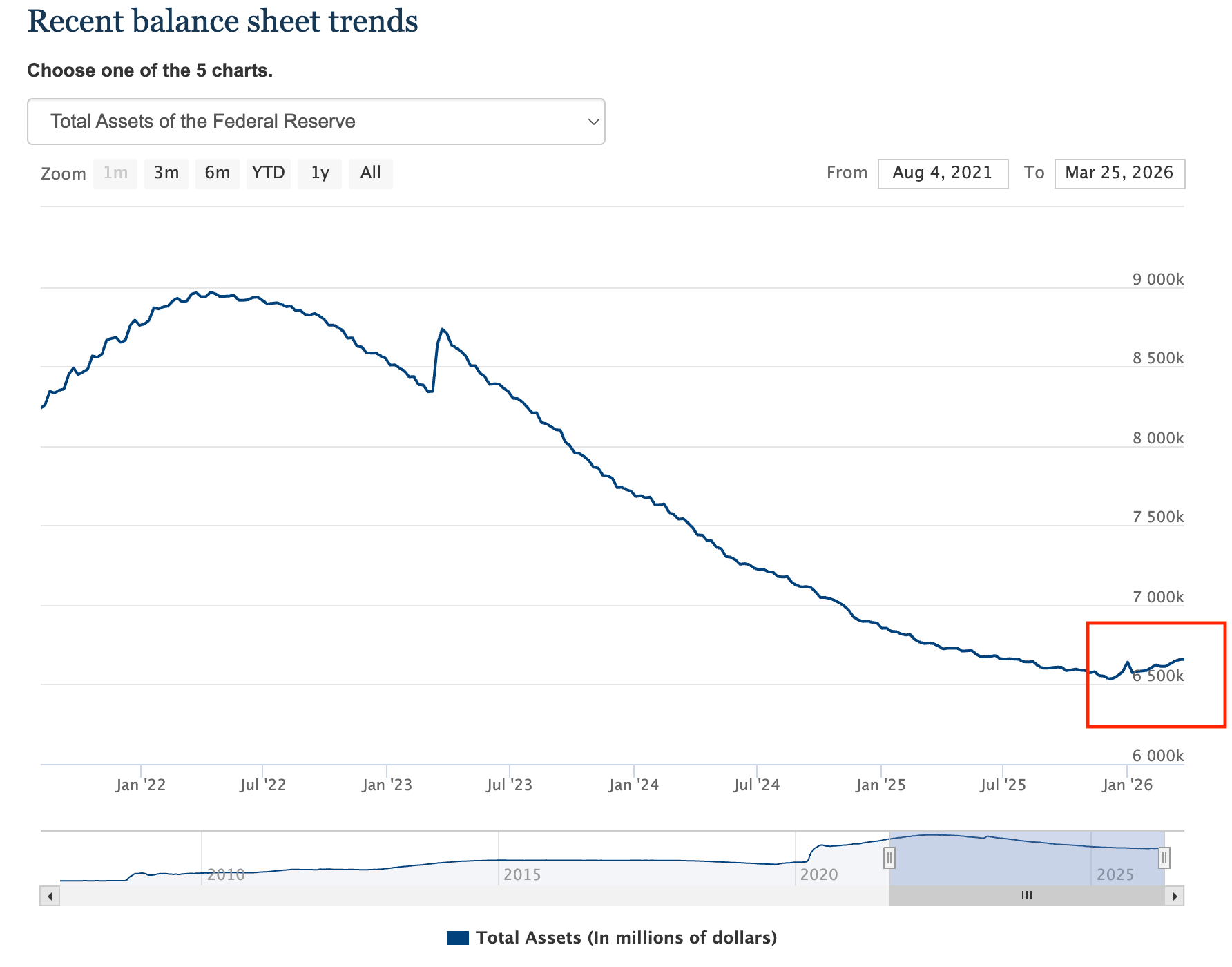

We also see this loose monetary policy in the increase in the Fed’s balance sheet.

This reveals that the central bank has relaunched quantitative easing (QE). Although you will never hear the term “quantitative easing” uttered by any Fed official, the central bankers quietly resumed QE in December.

So, it is true that inflation is heating up. It has been for quite a while. But it’s not fundamentally about the Iran War or rising oil prices.

The conflict will undoubtedly increase prices on a wide range of goods and services. It will exacerbate economic pain. And it could tip the world into a recession. But even if the war ends tomorrow and oil prices crash, we’ll still have an inflation problem because the government will continue to print money.

In fact, if they can convince you that the inflation threat is over when the oil price drops, they’ll be able to crank up the inflation machine even higher.

After all, they’ll need to print more money to support the borrowing and spending necessary to fight this war (on top of all the other spending).

Don’t be tricked by rosy CPI prints and financial media talking heads. Watch the money supply and plan accordingly.

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

{kind=link}