(Mike Maharrey, Money Metals News Service) I often see mainstream headlines touting the resilience of the American consumer. These stories almost always refer to strong retail sales figures signaling Americans’ willingness to keep spending money. However, there is a dark side to this spending pattern that often goes unnoticed.

There is a difference between spending because you can and spending because you have to. When prices rise, spending necessarily rises with them, and that’s exactly what is happening to the American consumer.

Rising retail sales figures aren’t inflation-adjusted, meaning they reflect both the number of items sold and the price of those items. When gasoline prices spike, retail sales necessarily spike right along with them. So, when the cost of everyday necessities rises, people have little choice but to spend more. After all, you still have to buy groceries and put gasoline in your car.

What is a cash-strapped consumer to do?

Drain your savings and turn to Visa and Mastercard.

This is exactly what Americans have done. They’ve blown through their savings and buried themselves in debt.

Blowing Through Our Savings

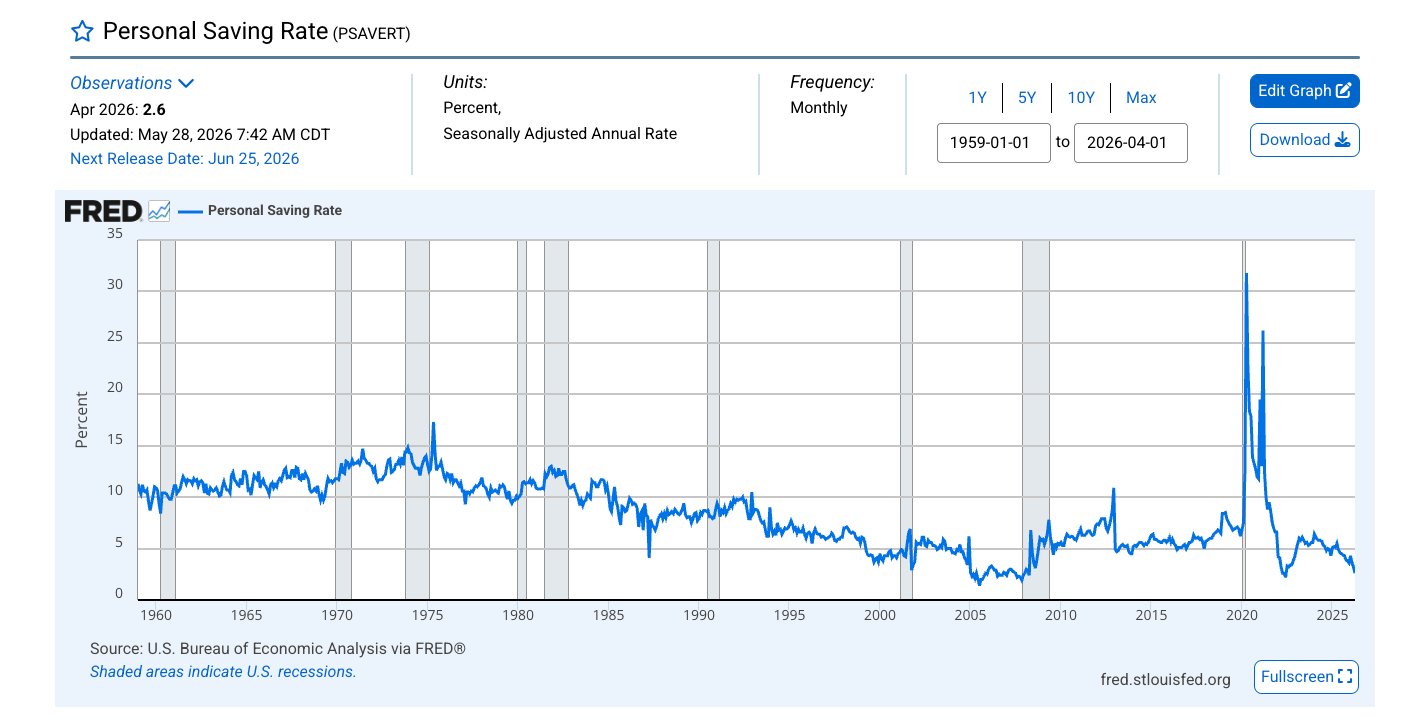

As Americans endured the COVID era locked in their homes, they managed to save a lot of money. In April 2020, the personal saving rate skyrocketed to 31.8 percent. It was by far the highest level since the 1960s.

Now the savings are gone.

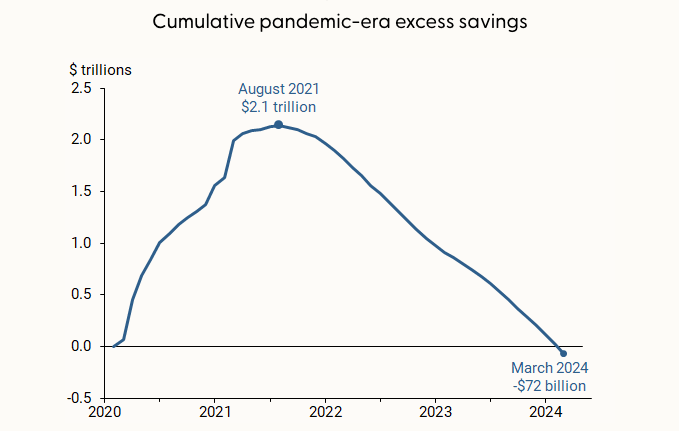

Aggregate savings peaked at $2.1 trillion in August 2021. By June 2023, the San Francisco Fed estimated that aggregate savings had dropped to $190 billion.

In other words, Americans blew through $1.9 trillion in savings in just two years.

By March 2024, the San Francisco Fed estimated that the entirety of those excess savings was gone.

And Americans aren’t replacing that savings cushion.

In April, the personal savings rate plunged to 2.6 percent. That’s the lowest level since just before the 2008 Financial Crisis and the Great Recession. It is getting close to the all-time low of 1.4 percent in July 2005.

Note that the savings crash preceded the Great Recession.

Burning Up the Plastic

So, what do you do when prices are soaring, you’ve tightened your budget as much as you can, and you still can’t make ends meet?

You pull out the plastic.

This explains why consumer debt is at a record level of $5.14 trillion. Revolving debt, primarily reflecting credit card balances, has surged to a record $1.4 trillion.

As Americans were beefing up their savings during the pandemic, they also paid down credit card debt. Revolving debt dropped below $1 trillion in 2020.

Mainstream analysts tend to look at various data points in isolation. They see strong retail sales numbers and immediately conclude the consumer is doing well. But when you start putting things together, a different picture emerges.

For instance, March retail sales surged by 1.5 percent as gasoline prices skyrocketed. Yay! But that same month, revolving debt also surged, growing by 9.1 percent. That seems to indicate that a large percentage of March’s surging retail sales were paid for with credit cards.

This does not scream “resilient consumer.” In fact, it smacks of desperation.

The big jump in consumer debt in March broke a trend of slowing debt growth. This may indicate that consumers are getting close to their credit limits.

American Consumers Under Stress

They are certainly struggling with the growing debt burden and higher prices.

U.S. credit card delinquencies spiked in April. According to the latest New York Fed data, 13.1 percent of credit card balances are at least 90 days overdue. That’s the highest level since the late stages of the Great Recession.

Serious credit card delinquencies have climbed by 5.5 percent since the third quarter of 2022. That’s a faster deterioration pace than what we saw during the 2007-2010 period.

According to NY Fed data, credit card balances ticked down in Q1 2026. This indicates that consumers have slowed their pace of debt accumulation (It’s hard to charge it when you’ve hit your credit limit) even as they are struggling to service their existing debt.

Lower-income Americans are feeling the biggest pinch. However, affluent areas are also charting a rise in delinquency.

LegalShield’s Consumer Stress Legal Index (CSLI) reflects the strain. As a spokesperson put it, “Financial strain has settled into a new normal for American households.”

The CSLI dipped in Q1 2026 compared to the fourth quarter of 2025. However, the index was 11.6 percent higher than a year ago.

According to the report, the quarter-on-quarter dip was “largely due to seasonal tax refund relief in the Consumer Finance sector.”

“The index remains at an elevated level consistent with sustained, broad-based financial distress.”

The LegalShield Bankruptcy subindex was up 2 percent in Q1, charting an 8 percent increase year over year. According to LegalShield, its bankruptcy data has historically served as a leading indicator, preceding actual non-business bankruptcy filings by two quarters with a .95 correlation since 2006.

The Foreclosure subindex was up 20.3 percent year-over-year. That was the highest level since the onset of the pandemic in March 2020. LegalShield called it “the sharpest signal of distress in the current economy.”

“Homeowners are facing severe payment shock driven by escrow resets. National homeowners’ insurance premiums rose 70 percent between 2019 and 2025, now accounting for 14 percent of the average monthly mortgage payment. The principal isn’t the problem; the total monthly obligation has quietly reset higher.”

So, when you see mainstream reports touting the “strong consumer,” take them with a grain of salt. Ask yourself, “What data points are they missing or just ignoring?” Because taken as a whole, the data points to a consumer at the end of his proverbial rope.

This underscores a broader point. An economy built on borrowing and spending money for stuff isn’t sustainable. At some point, consumers will crack under the pressure, taking this debt-riddled bubble economy down with them.

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

{kind=link}