(Mike Maharrey, Money Metals News Service) Since the Federal Reserve enacted its supersized rate cut in mid-September, the yields on 10-year and 30-year Treasuries have spiked.

I don’t think that was the plan.

After all, the point of a rate cut is to lower interest rates, not raise them.

This reveals a dirty little secret: the Fed can manipulate short-term interest rates by dictate, but it doesn’t have the same kind of control over long-term rates.

And this is a big problem for the federal government as it struggles with rapidly increasing borrowing costs.

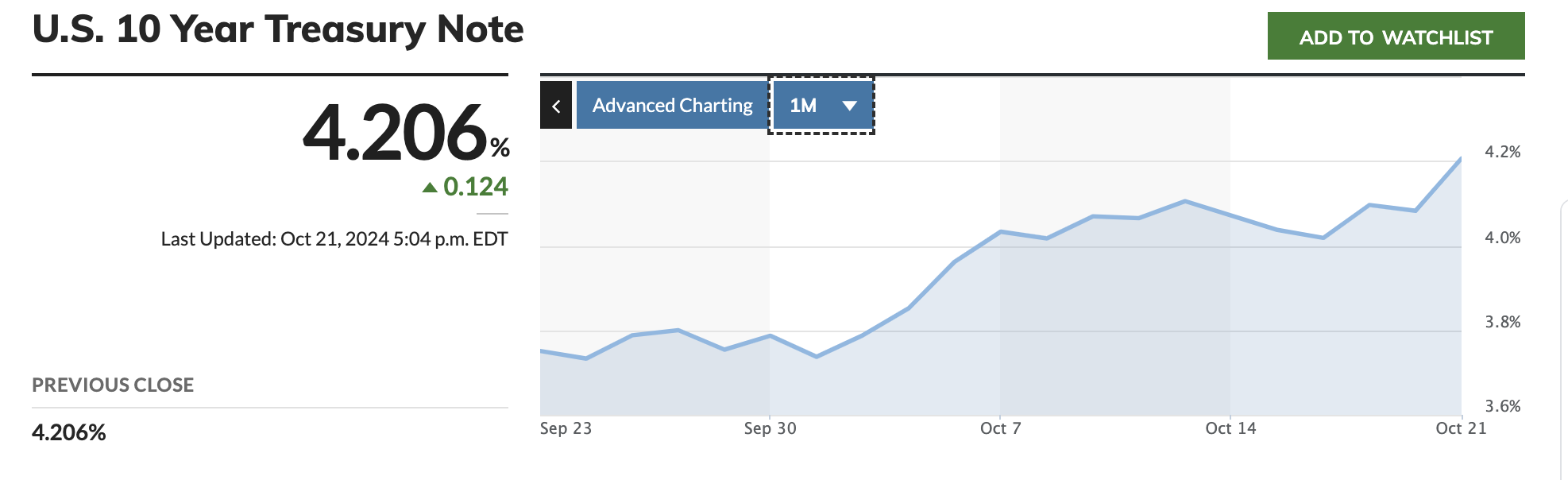

When the Fed announced its 50 basis-point rate cut, the yield on the 10-year Treasury was around 3.7 percent. On Monday (Oct. 21), the yield closed at 4.2 percent.

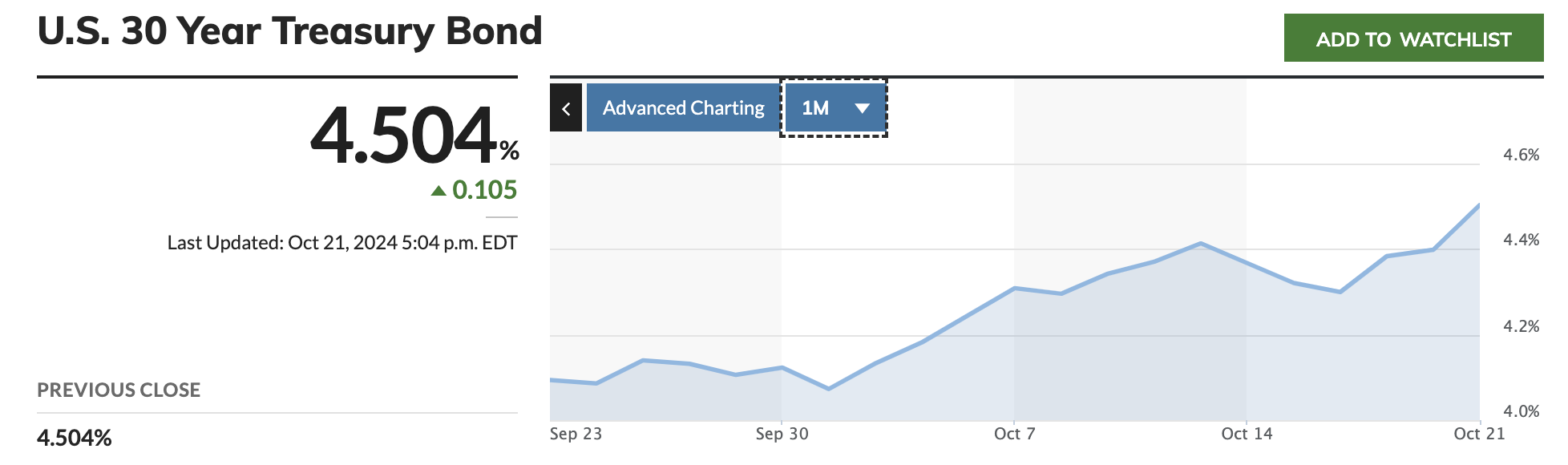

The 30-year yield was at 4 percent on the last day of the September Federal meeting. It has jumped to 4.5 percent on Monday.

This big jump in yields followed a temporary dip in rates after the Fed announced its rate cut.

It’s interesting to note that gold has continued to set new records despite the surge in bond yields. Historically, rising interest rates are a headwind for gold.

What’s Going on in the Bond Market?

Why have Treasury yields gone up even with the Federal Reserve trying to push interest rates lower?

The conventional wisdom is investors are now expecting the economy to be stronger moving forward. Therefore, the Fed may have to cut rates at a slower pace. This is certainly plausible, but given that the economy really isn’t all that strong (and a lot of that “strength” has been purchased with government borrowing and spending), it would behoove us to consider some other factors.

There are two other signals the bond market could be sending.

First, rising rates on the long end of the curve could indicate investors are worried about higher price inflation in the long term. When inflation expectations rise, investors demand higher returns on bonds in order to compensate for a depreciating dollar.

Second, rising bond yields could indicate sagging demand for U.S. debt.

Bond yields are inversely correlated with bond prices. When the demand for Treasuries softens, prices fall, and yields rise to entice more buyers into the market.

A Big Problem for the Federal Government

No matter what is causing it, rising bond yields are a big problem for Uncle Sam as he tries to finance the ever-growing federal budget deficits.

The federal government is already struggling with rapidly rising borrowing costs. The U.S. Treasury paid $1.13 trillion in interest expense in fiscal 2023. It was the first time interest expense has ever eclipsed $1 trillion.

Interest payments were up 28.6 percent over fiscal 2023 levels.

The U.S. government paid more in interest than it did for national defense ($882 billion) or Medicare ($874 billion). The only spending category larger than interest on the debt was Social Security ($1.46 trillion.)

I’m sure government people in Washington D.C. hoped the Fed’s pivot to rate cuts would relieve some of the interest pressure, but so far, that hasn’t happened.

It’s quite possible that the Fed won’t be able to lower federal borrowing costs with even with deeper interest rate cuts. As already mentioned, the central bank can move the short end of the rate curve, but it has a much harder time manipulating long-term rates. There are too many other contravening factors.

Ultimately, the federal government needs the Fed to step in and put its big fat thumb on the bond market. That would mean a return to quantitative easing (QE).

In QE operations, the central bank buys Treasuries on the open market. This increased (artificial) demand drives bond prices higher and puts downward pressure on yields. This would be an ideal scenario for the U.S. government. It needs all the help it can get to facilitate its borrow/spend addiction.

But the Fed runs QE operations with money created out of thin air. The new money gets injected into the monetary system and the economy. This is, by definition, inflation.

In other words, the Fed is between a rock and a hard place. It needs to get interest rates down for the Treasury (Fed officials claim they don’t care about the government’s fiscal issues, but I call BS.), but doing so runs the risk of reigniting price inflation, which isn’t exactly dead and buried.

Could We Be Heading for a Secular Bear Market in Bonds?

The rise of long-term Treasury yields in the face of interest rate cuts raises the specter of a long-term bear market in bonds.

This is exactly what analyst Jim Grant thinks is happening.

During an interview in the summer of 2023, Grant said he thought we were about to enter “a long cycle of rising interest rates” and a “generational” bear market in bonds.

“The great question of whether rates are mean or reverting? So, what characterizes interest rate movements is their generation length phasing, not necessarily cycles, but there are phases.

“Interest rates fell for the last quarter of the 19th century, rose for the first 20 years of the 20th, fell from 1920, ‘46 rose in ‘46 to ‘81, fell from ‘81 to, call it, 2021. So, at each juncture, there was some mark of excess, some mark of speculative excess blow-off. Certainly, in 1981, you know, a 20 percent-plus funds rate seemed excessive. A 14 percent yield in 1984 in long bond when the CPI was printing at four or five that seemed excessive. 10 percentage points of real yield — that seemed a lot.

“So, I speculate that we are embarked on a long cycle of rising rates. And I say that first of all, for reasons of pattern recognition, there’s no theory behind it. But I observe that in 2020 and ‘21, some unimaginably large number of debt securities were priced to yield less than nothing. Bloomberg keeps this particular figure. And I bet still, perhaps you could check me on this, I bet still, there’s like a hundred billion of bonds priced to yield less than nothing worldwide. But there were $18 trillion, I think, at the peak.

“[It was] the most extraordinary expression of unqualified bullishness on an asset class because it had the name of ‘bonds’ which had been falling in yield, rising in price. So no, it would not surprise me at all if we were embarked on something resembling a generation-length bear market in bonds, meaning rising yields and falling prices that would fit the form.”

As already explained, a long-term bear market in bonds would be a disaster for the federal government.

Whether or not Grant is correct remains to be seen, but there is no doubt yields are rising despite the Fed’s best effort, and that should at least raise eyebrows.

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

, the yield closed at 4.2 percent.){kind=link}