(Mike Maharrey, Money Metals News Service) In a year of massive deficits, the Biden administration ran the biggest deficit of the year in August.

Meanwhile, interest on the national debt eclipsed $1 trillion for the first time.

The August budget shortfall came in at $380.08 billion, according to the latest Treasury Statement. That pushed the fiscal 2024 deficit to $1.9 trillion with one month left to go. The Biden administration has already spent its way past last year’s $1.7 trillion shortfall.

We’re seeing these huge spending levels and massive deficits despite what is supposed to be a “strong” economy. Imagine what the deficits will look like when the economy tanks.

The Treasury reported $306.54 billion in receipts in August. That was an 8.3 percent revenue increase compared to August 2023.

Last month’s year-on-year revenue increase wasn’t an anomaly. It’s happened consistently all year. To give you an idea of how well the Treasury is doing, in April, Uncle Sam ran a surplus thanks to tax day. Tax receipts came in at $776.2 billion in April, a 22 percent increase over last year.

This obliterates the idea parroted by Democrats that the deficits are because of tax cuts. The real problem is on the spending side of the ledger.

To say the Biden administration is spending like a drunken sailor would insult drunken sailors.

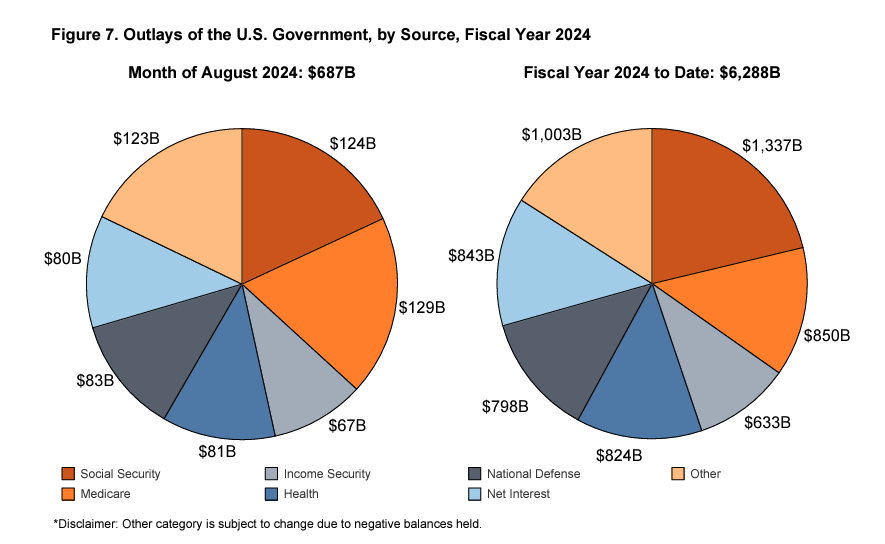

Last month, the federal government blew through $686.62 billion.

That number was somewhat inflated because some September payments were pushed back into August with September 1 falling on a Sunday. That could mean a slightly lower spending total in September – maybe.

Federal spending in fiscal 2024 stands at $6.29 trillion. That’s already 2.6 percent higher than last year with a whole month of spending left.

Remember how the Biden administration promised that the [pretend] spending cuts would save “hundreds of billions” with the debt ceiling deal (aka the [misnamed] Fiscal Responsibility Act)?

As you can see, that never happened. That should tell you something about government promises when it comes to spending.

Don’t think I’m just picking on Biden and the Democrats. They just happen to be the ones currently driving the car toward the cliff. Things weren’t much better when Trump was at the wheel.

Before the pandemic, the U.S. government had only run budget deficits of over $1 trillion four times — all by the Obama administration in the aftermath of the 2008 financial crisis.

The Trump administration almost hit the $1 trillion mark in 2019 and was on pace to run a trillion-dollar deficit in fiscal 2020 before the pandemic, even as the U.S. supposedly enjoyed the “best economy” ever. The economic catastrophe caused by the government’s response to COVID-19 gave policymakers an excuse to spend with no questions asked and we saw record deficits in fiscal 2020 and 2021.

This reveals the ugly truth; borrowing and spending is a bipartisan sport. No matter who is in power or what you hear about spending cuts in Washington D.C., the federal government always finds new reasons to spend more and more money. Whether it’s a disaster, an emergency, or somebody else’s war, the spending train never reaches the station.

The Interest Problem

Spiraling debt and higher interest rates are creating a double whammy that is on the verge of overwhelming the federal budget.

Last month, the U.S. government spent $92.29 billion just paying interest on the national debt. That drove the total interest expense this year over $1 trillion for the first time in history. Interest expense this year is nearly 30 percent higher than last year and makes up about 23 percent of total revenues.

Last month, the federal government spent more on interest expense than it did on National Defense ($89 billion). The only spending categories that were higher were Social Security and Medicare.

And interest expenses will only continue to climb.

Much of the debt currently on the books was financed at very low rates before the Federal Reserve started its hiking cycle. Every month, some of that super-low-yielding paper matures and has to be replaced by bonds yielding much higher rates.

Anybody who says “deficits don’t matter” is deluded.

And the only way out of this fiscal death spiral is significant spending cuts and/or major tax hikes.

I wouldn’t hold my breath.

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

{kind=link}