(Mike Maharrey, Money Metals News Service) The movement of silver out of the U.S. has helped ease market tightness, but an ongoing structural supply deficit makes the metal vulnerable to future squeezes.

Silver went on an incredible run late last year after taking off in October as a silver squeeze gripped the market. The metal opened in 2025 at $28.84 and didn’t crack $40 until September. When the year ended, the price sat at $71.30. At its peak, silver was up 147 percent intra-year. The average price came in at $40, a 42 percent increase.

A convergence of factors, from market dynamics to logistical problems, led to the October squeeze, and to a second squeeze late last year that briefly drove silver prices over $100 in January.

The Silver Shortage

While the market dynamics that got us here might be difficult to untangle, the situation is about as basic as it gets.

There’s not enough silver.

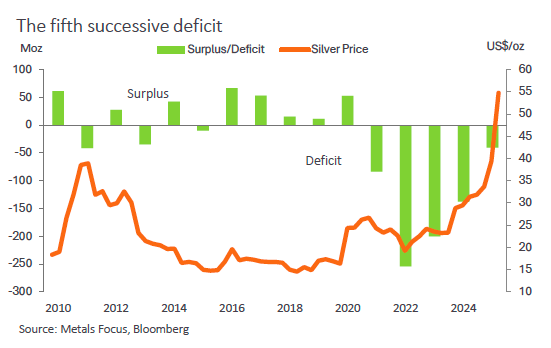

The silver market recorded a supply deficit for the fifth consecutive year in 2026.

Last year, demand outstripped supply by 40.2 million ounces (1,252 tonnes). That drove the 5-year market deficit to 716 million ounces. To put that into perspective, total silver mining output last year was 846 million ounces. Metals Focus forecasts a 46.3-million-ounce supply deficit this year.

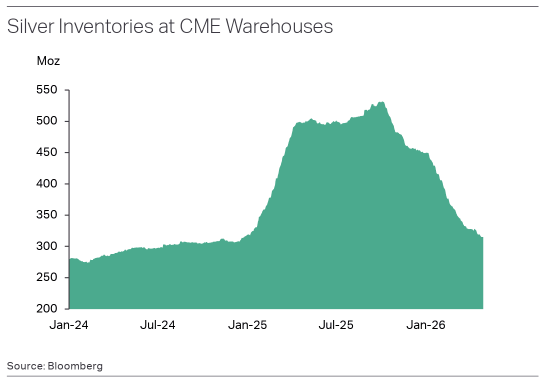

The stage was set months earlier when tonnes of silver moved from London to New York due to tariff worries. As President Trump began levying tariffs in April 2025, silver streamed into the U.S. CME silver holdings, eclipsing the record set during the pandemic at 531 million ounces.

The stage was set months earlier when tonnes of silver moved from London to New York due to tariff worries. As President Trump began levying tariffs in April 2025, silver streamed into the U.S. CME silver holdings, eclipsing the record set during the pandemic at 531 million ounces.

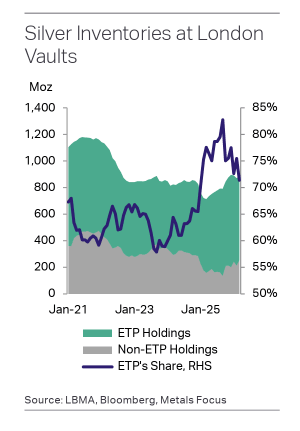

Meanwhile, metal bled from London vaults.

Much of the silver remaining in London was already committed to ETFs. That left very little “free float” metal to provide liquidity to the London market. According to Metals Focus, the share of London silver stocks, not allocated to ETPs, fell to just 17 percent by the end of September 2025.

That set the stage for the first squeeze, and a surge in Indian silver demand last fall was the pin that popped the bubble.

Initially, Indian buyers were primarily sourcing silver from Hong Kong, but they reportedly shifted more toward London during the Chinese Golden Week Holiday in the first week of October.

But London vaults were already tapped out.

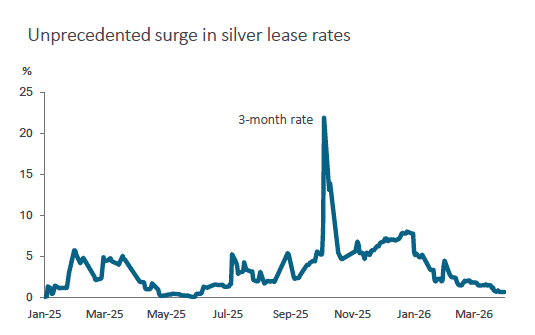

As the squeeze intensified, silver lease rates exceeded 200 percent, reflecting the strain in the market.

After a healthy correction in January, the market has stabilized, with silver prices settling in a range between $70 and $80 an ounce.

Metal Movement Provides Some Relief

The movement of silver out of the U.S. helped to settle the market.

After peaking at 531.9 million ounces in October, CME silver inventories recorded sustained withdrawals. According to Metals Focus, CME stocks stood at 315.2 million ounces at the end of last month. That’s comparable to inventories back in November 2024. In effect, all the tariff-driven inflows between December 2024 and October 2025 have been unwound.

According to Metals Focus, “Physical tightness, easing EFP spreads and rising regional premiums have all incentivized the movement of silver out of CME vaults.”

Analysts also noted that the Trump administration has refrained from levying tariffs on precious metals (so far) and has been negotiating with “key partners.”

“This more dovish stance has, at least for now, alleviated tariff concerns.”

U.S. export data also reflects the movement of silver out of the U.S. In just the first two months of 2026, 95 million ounces of silver flowed out of the United States. That exceeds annual silver exports over the last several years.

About half of that metal went to London. However, there was a significant increase in silver exports to the UAE and Hong Kong. According to Metals Focus, imports from the U.S. to both regional hubs in January and February were equivalent to multi-year cumulative totals.

“This aligns with market feedback suggesting that a surge in investment demand in early 2026 was geographically broad-based. … Growth in East Asia and the Middle East (regions where physical investment has historically been subdued) was exceptionally strong in early 2026, although buying has moderated since March.”

While more than half of the silver flowing to the U.S. went to London, metal held in commercial vaults there dropped by 1 percent, indicating that the country is serving as a pass-through to other markets. Metals Focus analysts said, “This largely reflects acute bullion supply shortages in certain markets in early 2026 following a surge in physical investment.”

“As regional liquidity tightened, traders increasingly drew on London stocks, with the Middle East and East Asia once again among the top destinations for UK silver exports. As a result, the UK was a net exporter of silver bullion in the first two months of the year, although a reversal has been evident since March.”

While the amount of silver in London vaults has barely budged this year, the amount of “free float” silver available for trading or delivery has increased as metal committed to ETFs dropped after the price correction. Global silver ETF holdings have declined by around 70 million ounces (5 percent) year-to-date.

Currently, the amount of free float silver in London stands at around 235 million ounces, the highest level since December 2024. That’s up approximately 116 million ounces since the low last September.

There’s a High Risk of Additional Silver Squeezes

While the shuffling metal between the U.S., London, the Middle East, and Asia has taken the strain off the silver market, it has not solved the fundamental problem.

As already noted, there isn’t enough silver.

It’s like a game of musical chairs. Everything seems fine while the music is playing. However, when it stops, there are going to be problems.

Metals Focus analysts said the silver market is still at risk for additional squeezes.

“At the time of writing, the physical silver market appears closer to historical norms, as evidenced by a further decline in leasing rates in recent weeks. However, global identifiable inventories remain low compared to levels seen in the early 2020s. More importantly…the silver market is expected to remain in a fundamental deficit in 2026, at a level similar to that recorded in 2025.”

Analysts noted that the prospect of improving investment demand later this year “implies a continued cumulative drawdown of stocks.”

“As a result, the market remains vulnerable to periodic liquidity squeezes. While such events will remain uncommon, structurally lower liquidity than in previous years suggests that price and lease rate volatility will persist.”

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

. That drove the 5-year market deficit to 716 million ounces. To put that into perspective, total silver mining output last year was 846 million ounces. Metals Focus forecasts a 46.3-million-ounce supply deficit this year.){kind=link}