(Mike Maharrey, Money Metals News Service) There is no government report more meaningless and yet more relied upon by policymakers than the monthly non-farm payroll report released every month by the Bureau of Labor Statistics.

Every month, the BLS releases data. Every month, we get breathless headlines about the “strength” or “weakness” of the economy based on this data. Every month, policymakers pore over the job report as they make decisions about the trajectory of monetary policy.

And every month, the BLS revises the previous month’s data.

It happened again in March.

The mainstream financial media trumpeted the “surprisingly strong” job gains, as the economy posted the largest jump in new jobs in 15 months. This drove headlines like this:

Fed rate cut hopes collapse.

Because, you see, a strong economy with lots of jobs means the Fed can keep interest rates higher for longer.

Markets were closed due to Good Friday. However, gold would almost certainly have sold off based on this jobs report. (I’m writing this over the weekend, and I will be shocked if gold doesn’t sell off on the news on Monday – barring a significant war headline.)

The forecast was for 59,000 news jobs in March. According to the BLS data, the economy added 178,000 jobs.

That’s great, right?

The unemployment rate also ticked downward to 4.3 percent. This was primarily due to a sharp reduction in the overall labor force. According to the data, the number of working-age Americans in the labor force fell to 61.9 percent, the lowest since November 2021.

Taken at face value, this is a tremendous jobs report. It indicates a resilient economy.

However, you can’t take BLS data at face value. It’s almost certain that these “blockbuster” numbers will be revised.

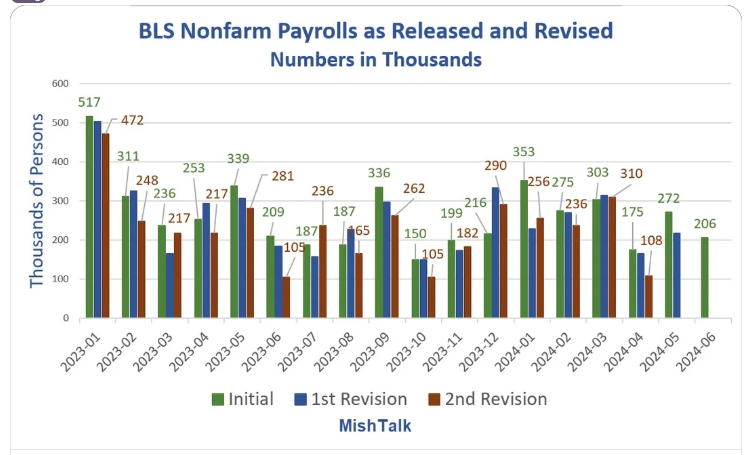

In fact, there were revisions in the March report, erasing a total of 7,000 jobs from the last two months.

Shockingly, January data was revised up (a rare occurrence, as I will soon show), with the BLS adding 34,000 jobs. That pushed the January number to 160,000 jobs.

However, the BLS erased 41,000 jobs from the February data. That means the economy lost -133,000 jobs that month. It was the worst drop in jobs since December 2020 in the midst of the pandemic.

Averaging the data from the last three months, the economy is adding around 68,000 jobs per month – at least until they revise the numbers some more.

Revisions Are the Norm

Regardless, the numbers are never really the numbers. They change month after month as the analysts at the BLS fidget with their slide rules and abacuses

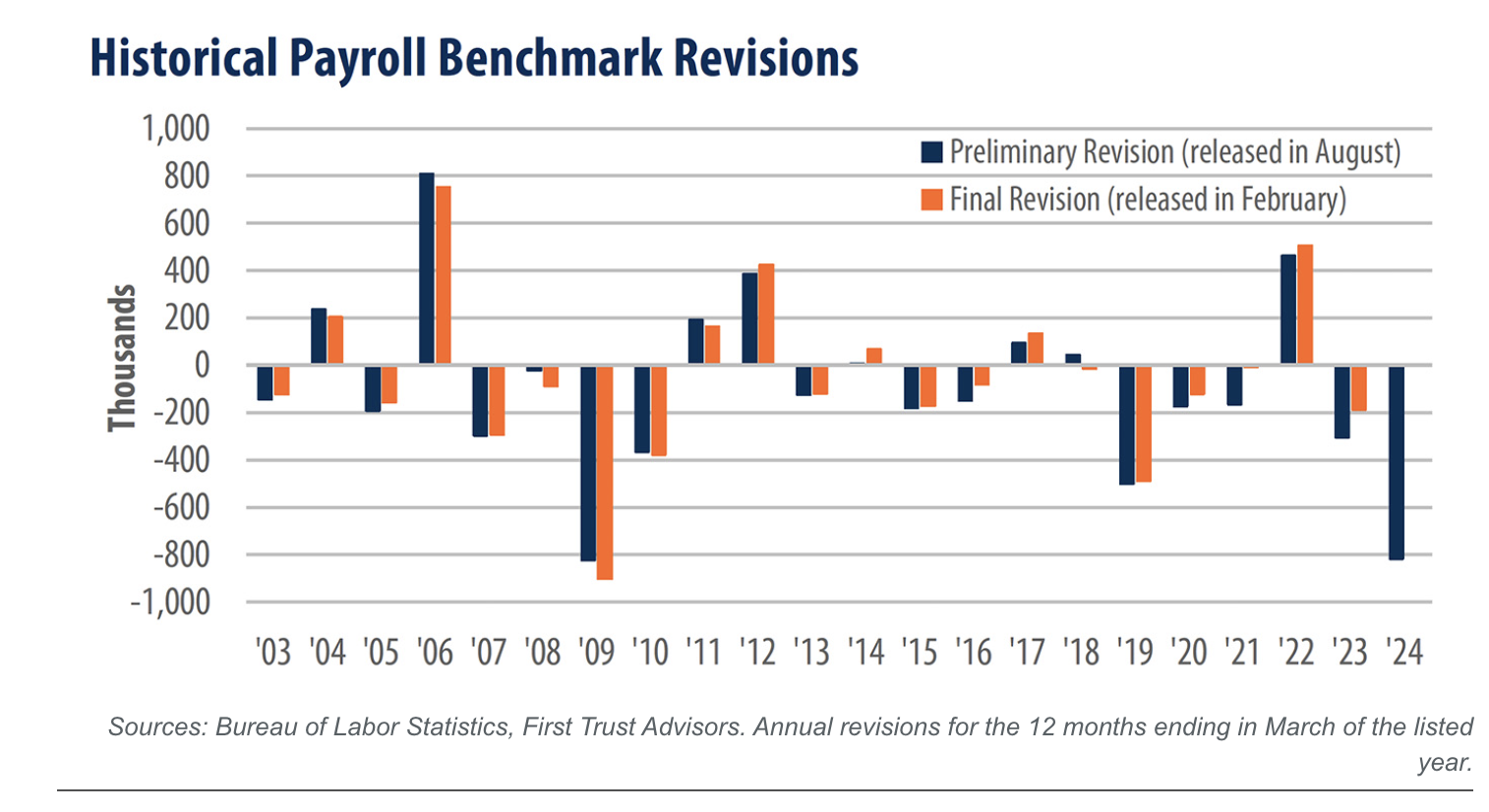

Keep in mind, in January, the bureau made its end-of-the-year adjustment to the “birth-death model” it uses to determine job growth. That erased nearly half a million jobs from the economy. To be precise, the BLS wiped out 403,000 jobs with its model revision. (At the same time, it revised December’s report down from 50,000 to 48,000 jobs.)

With that revision, the U.S. economy only generated an average of 15,000 jobs per month in 2025. You probably don’t have that impression if you just saw the headlines as the BLS announced its employment data each month.

If it sounds like the agency is just making stuff up, well…

And even if you give the folks over at the BLS the benefit of the doubt and assume they’re doing the best they can, their best is pretty abysmal.

In fact, downward revisions are standard operating procedure for the BLS. The agency erased nearly 1 million (911,000) jobs that it initially claimed were created between March 2024 and June 2025.

So, what are we to make of the March report claiming the economy added a surprising 1780,000 jobs?

Absolutely nothing.

Because some of these jobs will almost certainly be erased next month.

The BLS has a long history of reporting rosy job numbers only to quietly come back and revise them downward down the road. In 2023, job numbers were revised down in 10 of the 12 months.

To be fair, compiling employment data is no simple task. Revisions should be expected. But why do the updates almost always remove jobs from the economy? One would think you’d see upward revisions nearly as often as downward, right?

Nope.

Since 2003, the final annual BLS numbers were lower than the initial report 14 times compared to seven upward revisions.

That being the case, who really cares what this report says?

Well, pretty much everybody, because despite the sketchy nature of the data, the jobs report is probably the most anticipated, analyzed, and quoted data release by the federal government, with the possible exception of CPI and GDP data.

This is a problem given the nature of the data.

It’s notable that markets only react to the initial numbers. You never see markets tank because the BLS erased a bunch of jobs from the economy with a few clicks of its calculator. The revisions happen quietly in the back alleys. Nobody pays any attention to them. That creates the illusion that the labor market is much stronger than it is.

It goes something like this:

This month, the government reports good news. Everybody celebrates. Markets move. The following month, the government quietly revises everything downward and reports that the good news was really bad news.

And nobody pays attention.

This wouldn’t matter nearly so much if central bankers and government officials didn’t lean so much on this data to make decisions. But they do. And if the data is this unreliable, what does that tell you about the decisions based on this data?

Let’s be honest – when you look at the history, one’s got to wonder why anybody takes these numbers at face value.

The lesson here is that we need to be somewhat skeptical of government data. And we need to pay attention – not just to the headline release, but the revisions as well.

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

{kind=link}