(Mike Maharrey, Money Metals News Service) Jerome Powell says the economy is in “solid shape.” Jerome Powell says inflation is still elevated. Jerome Powell says he doesn’t see a recession risk.

And yet the Federal Reserve just supersized its rate cut, indicating that the central bankers are more worried about the impact of higher interest rates on this debt-riddled, bubble economy than they’re letting on.

And as the saying goes, actions speak louder than words.

What the Federal Reserve People Did

As expected, the FOMC wrapped up its September meeting by announcing an interest rate cut. It was the first cut since 2020.

However, somewhat unexpectedly, the Fed committee went big and slashed rates by half a percentage point, setting the federal funds rate in a range between 4.75 and 5 percent.

While there was growing speculation that the FOMC might go for a 50-basis point cut, most analysts expected the central bank to ease into easing with a 25-basis point cut.

The FOMC also indicated that it plans to cut further.

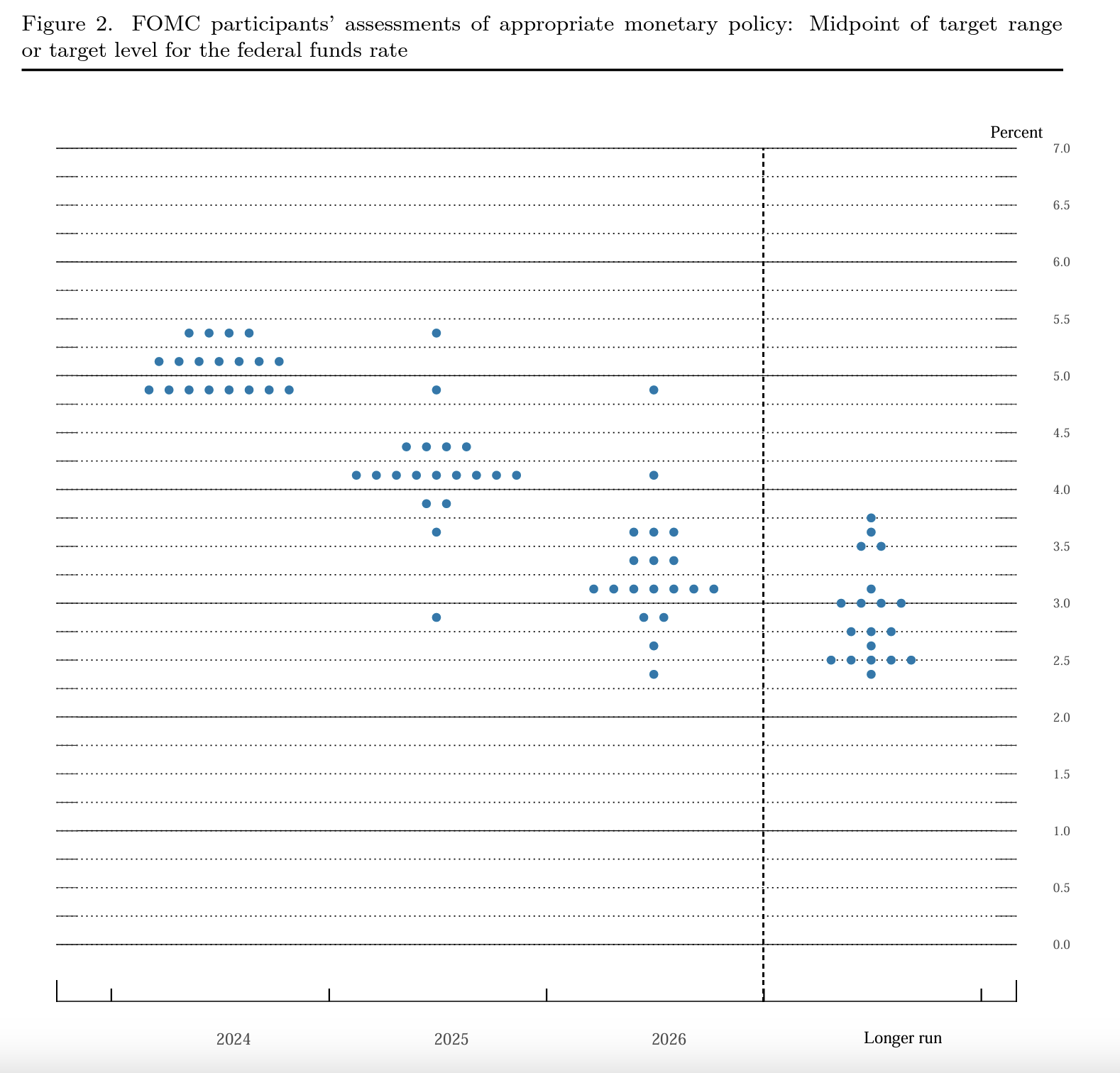

Based on the newly released “dot plot” showing the expected trajectory of interest rates, 17 FOMC members indicated they expected further cuts this year, with the rate coming down to 4.4 percent. That would mean another half-percent cut this year.

The committee also projects further cutting in 2025, with rates dropping to 3.4 percent. This is lower than the 4.1 percent projection in the last set of dot plots.

I should note that these projections are notoriously bad.

How bad?

Fund manager David Hay analyzed past dot plots and found the FOMC only got interest rate projections right 37 percent of the time. And as Hay pointed out, “They control interest rates!”

For instance, in March 2021, the FOMC projected the interest rate would still be zero in 2022. The actual 2022 rate was 1.75 percent. And in 2023, the vast majority of FOMC members thought the rate would still be at zero. The actual rate was over 5 percent.

What the Federal Reserve People Said

Even as they supersized the interest rate cut, Powell & Company talked about an ongoing elevated inflation risk and a strong economy.

The official FOMC statement noted, “Inflation has made further progress toward the Committee’s 2 percent objective but remains somewhat elevated.”

As far as the economy, Powell & Company spun a positive narrative. The FOMC statement said the economy is continuing “to expand at a solid pace,” and Powell downplayed the possibility of a recession – or an economic downturn.

“I don’t see anything in the economy right now that suggests that the likelihood of a recession, sorry, of a downturn, is elevated. I don’t see that. You see growth at a solid rate. You see inflation coming down. You see a labor market that’s still at very solid levels. So, I don’t really see that now.”

Powell characterized the Fed’s rate cut move as a “Goldilocks” policy – just right.

“This recalibration of our policy stance will help maintain the strength of the economy and the labor market and will continue to enable further progress on inflation as we begin the process of moving toward a more neutral stance. We are not on any preset course. We will continue to make our decisions meeting by meeting.”

Powell reiterated that “our job is to support the economy on behalf of the American people,” and he assured us, “If we get it right, this will benefit the American people significantly.“

If.

Powell said we shouldn’t expect the ultra-low interest rates that characterized the decade after the 2008 financial crisis. He said the “neutral rate” is higher than it was back then.

“Intuitively, most — many, many people anyway — would say we are probably not going back to that era where there were trillions of dollars of sovereign bonds trading at negative rates, long-term bonds trading at negative rates.”

Of course, it’s easy to say that now. We’ll see what happens when the central bank faces the next economic crisis – which, despite the rate cut, is still barreling down the tracks.

Their Actions Don’t Match Their Words

When you put the Fed’s actions and the central bankers’ words together, it doesn’t make a lick of sense.

Principle Asset Management chief global strategist Seema Shah told CNBC that a 50-basis point rate cut with no sign of economic turmoil is “a unique move in history.”

In fact, the last two times the Fed started an easing cycle with a half-percent rate cut, it was a prelude to a crisis.

In January 2001, the Fed cut from 6.5 percent to 6 percent. Over the next year, the S&P 500 crashed by 39 percent, and unemployment skyrocketed, leading into a recession.

In September 2007, the Fed cut rates from 5.25 to 4.75 percent. A year later, we had the financial crisis and the Great Recession.

While Powell and Company are saying the economy is strong and inflation isn’t quite beat, they’re acting like they don’t care about inflation at all, and we are in the midst of an economic downturn.

At the least, the central bankers are worried about an economic crash.

Simply put, you don’t aggressively ease monetary policy in a booming economy.

But the markets were pleased that the easy-money drug has started flowing again. Shah called it a cause for celebration.

“We have a Fed that will go to historic lengths to avoid a hard landing. Recession, what recession?”

If by “historic lengths,” she means surrendering to inflation, she’s right.

Because that’s exactly what the Fed did; it waved the white flag and sounded the retreat trumpet.

Even before the rate cuts, the Fed was already winding down the inflation fight. The central bank loosened monetary policy when it quietly announced that it would begin to taper balance sheet reduction in June.

The balance sheet serves as a direct pipeline to the money supply. When the Fed buys assets – primarily U.S. Treasuries and mortgage-backed securities – it does so with money created out of thin air. Those assets go on the balance sheet, and the new money gets injected into the economy.

This expansion of the money supply is, by definition, inflation.

If expanding the money supply is inflationary, it logically follows that to slay price inflation, the Fed needed to significantly shrink the balance sheet. Rate hikes aren’t enough to ring all the liquidity out of the economy. In other words, if the Fed was serious about taming inflation, it would be talking about additional rate hikes and ramping up efforts to reduce the size of the balance sheet. It needs to undo the money creation of the past decade-plus.

I didn’t, and it won’t.

If the Fed was all in on the inflation fight, it wouldn’t be “recalibrating policy” to create more inflation.

Keep in mind – inflation is an expansion of money and credit. Price inflation is one symptom of inflationary policy.

The Fed has tightened things up just enough to slow rising prices, but as we can see from the balance sheet, most of the inflation created during the pandemic is still sloshing around in the economy. And that’s on top of all the inflation it created in the wake of the 2008 financial crisis that the central bank never managed to wring out of the economy.

But by slowing balance sheet reduction and super-sizing its initial rate cut, the Fed is telling you it plans to ramp up the inflation machine.

And why would it do that?

Because, while they won’t say it out loud, the central bankers know the economy is addicted to easy money. They know the economy can’t function in a higher interest rate environment. (In fact, 5.5 percent is close to “normal” from a historical perspective.) And they know that they have probably already broken things in the economy.

I’m not the only one who realizes the Fed’s actions signal the central bankers aren’t telling us the full story. Nomura Capital Assets analyst Matthew Rowe told Reuters, “Many market participants see this as an aggressive move that is not justified by what normal market participants can see.”

And he asked the operative question:

“So, what is it that they see, and we cannot, that would spur this level of aggressive action.”

The Fed people are clearly trying to get out in front of the damage they have caused. (They caused it when they held rates artificially low for more than a decade – not when they raised rates.) They’re telling you that everything is great. But their actions speak louder than their words.

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

They’re telling you that everything is great. But their actions speak louder than their words.){kind=link}