(Mike Maharrey, Money Metals News Service) When you watch the gold price all day, every day, you start to pick up on trends intuitively. Since gold corrected in January, I’ve noticed it often rises in the early morning and then drops as soon as the U.S. market opens. This would seem to indicate that demand for gold is generally stronger during Asian sessions and weaker in the West.

Turns out that my perception is the reality.

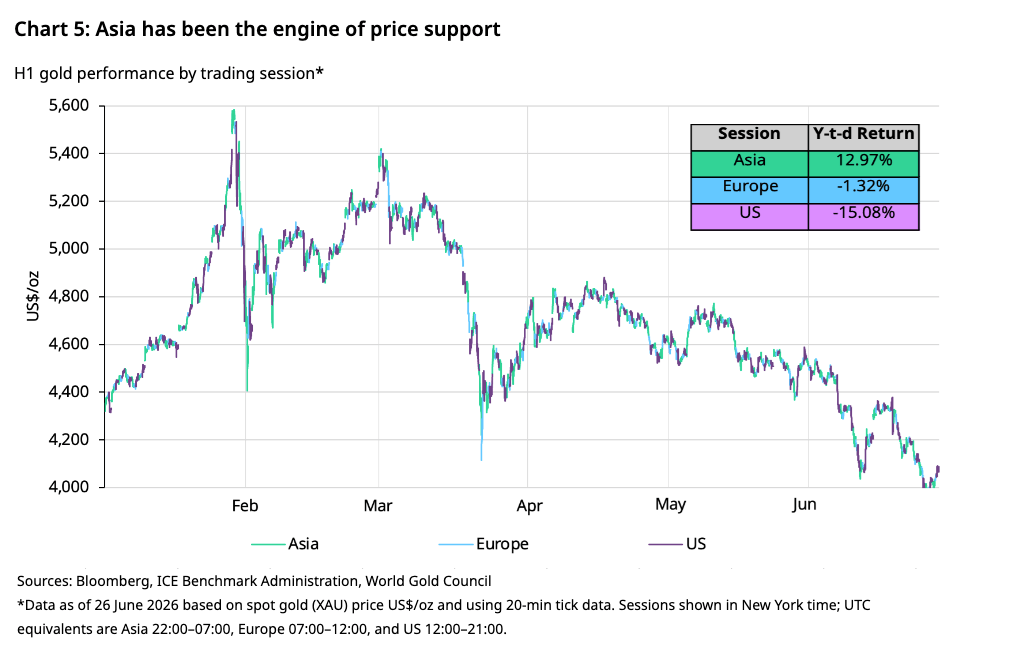

Buried at the end of the World Gold Council’s H1 gold market summary was an interesting chart that breaks down gold’s price movement by trading session. This data reveals that North American investors are driving the sell-off, while Asian investors are buying the dips.

In fact, the World Gold Council called Asia “the engine of price support.”

“Interestingly, intraday analysis suggests that the bulk of gold’s movements have been linked to activity during Asian and U.S. trading hours. Many of the pullbacks occurred during US hours and, conversely, gold’s rebounds generally occurred during Asian hours.”

During Asian trading hours, gold was up 12.9 percent through the first six months of the year. During North American trading hours, the yellow metal was down 15 percent. European sessions split the difference, with gold falling modestly by 1.3 percent.

Asia Supported the 2025 Bull Market

Asian investors, along with central bank gold buying, were the primary drivers during the early stages of this gold bull market.

Chinese buying helped push gold bar and coin demand to a 12-year high of 1,374.1 tonnes last year. In value terms, global bar and coin demand was a record-breaking $154 billion.

More than half of last year’s global coin and bar demand came from two countries – China and India.

The split between East and West becomes even more stark when looking at the data for the first half of last year.

Chinese bar and coin demand grew by 44 percent year-on-year in H1 last year as investors snapped up 115 tonnes of gold bars and coins in the second quarter alone. It was the strongest H1 for physical gold buying since 2013.

Meanwhile, Americans continued to sell their gold. Year-on-year bar and coin sales plummeted by 53 percent in H1. Demand in the second quarter was only 9 tonnes, the lowest quarterly level since Q4 2019.

Asian Markets Have Out-Bulled the West for Decades

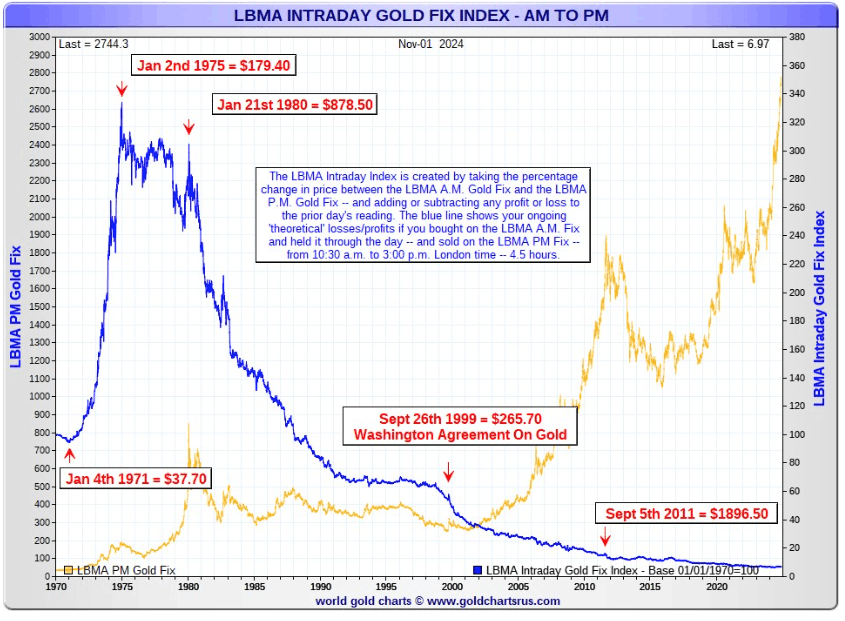

As it turns out, this phenomenon of gold rising during Asian trading hours and falling during North American sessions is not limited to the recent past. If you only invested at the London morning gold fix (10:30 a.m. GMT/5:30 EDT) and sold shortly after the P.M. price fix (3 p.m. GMT), you would gain very little. But if you bought at the P.M. fix and sold in the morning, you’d be up substantially.

Analyst Ed Steer ran the numbers.

“This first chart shows what happened to your $100 investment if you’d bought at the 10:30 a.m. GMT morning gold fix in London — and then sold it at the 3:00 p.m. GMT afternoon gold fix starting on the first trading day of January 1970…then reinvested that $100…plus or minus any gains or losses…the following day at the morning gold fix — and sold again at the p.m. fix once again.

“If you did this every business day for 54 years, your initial $100 investment would be worth US$6.97 today. Of course, that doesn’t include the loss due to currency debasement over that time…so in other words, you lost everything.”

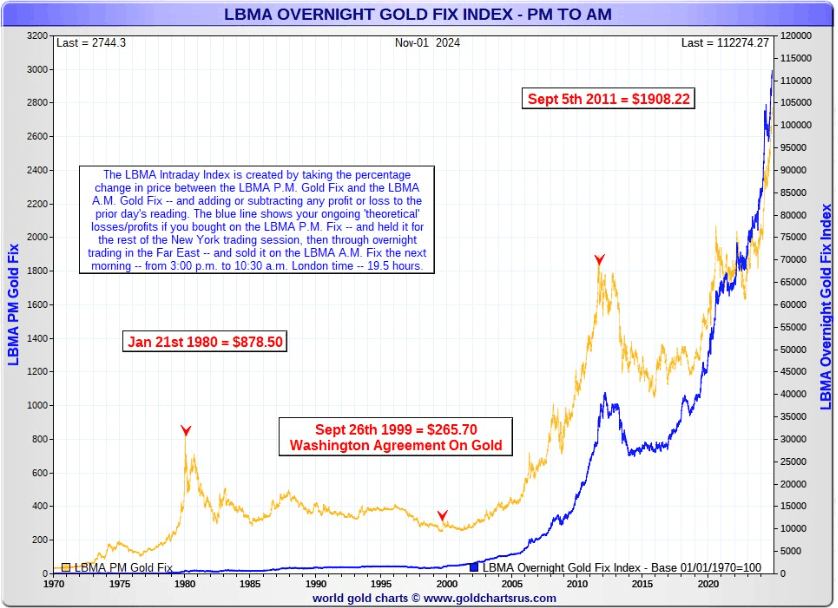

Conversely, if you’d invested $100 at the afternoon gold fix in London, held that investment until early in the Far East Globex trading session overnight — and then sold at the morning gold fix in London, the chart looks like this:

“As of the close of trading on 01 November 2024…that theoretical $100 invested 54 years ago had morphed itself into $112,274.27.”

Asia’s Lover Affair With Gold and Western Price Manipulation

This data underscores two important market realities.

First, Asians love gold even as Western investors tend to spurn it. As a result, gold is flowing from the West to the East. As Americans sell the yellow metal, Asians take advantage of the price dips and gobble it up.

Second, the data may hint at price manipulation by big Western banks, as Steer noted in his analysis.

“This simple difference in investment strategy is all the proof needed that the world’s banks and large commercial traders are actively managing the price between the a.m. and p.m. gold fixes in London — and have been doing so since the paper market in gold first opened on 02 January 1975.”

The paper market makes this kind of manipulation possible. The fact that there is far more paper gold than physical metal allows big banks to move paper quickly and en masse, and nudge the price lower. This type of manipulation is even more effective in the less deep silver market.

Steer argues that due to this tinkering, nobody knows the true free-market price of gold.

“But one thing is for sure is that they are many, many multiples of what they’re trading at today…silver in particular, as you already know.”

Interestingly, the Asian market is much more oriented around physical metal, with paper taking on a smaller role. As a result, Asian trading likely comes closer to representing a free market price than the London gold fix.

It’s impossible to know how much of this trend is due to manipulation and how much is simply a function of higher gold demand in Asia. However, the center of gold’s gravity is clearly much closer to Beijing than New York.

Meanwhile, Asian hubs, including Singapore and Hong Kong, are positioning themselves to take a more significant role in the global gold market.

Hong Kong recently launched a gold settlement system to challenge Western dominance. The government-owned clearing system will reportedly “mirror” the financial infrastructure used by the LBMA in London and will include a Hong Kong ticker (HAU). According to a spokesperson, the ticker will “ensure that Hong Kong gold prices are fully accessible to global market participants.”

It will be interesting to see how a more active Asian role in the market impacts the global dynamics. It may well make it more difficult for the powers-that-be in the West to control the price.

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

{kind=link}