(Mike Maharrey, Money Metals News Service) Since the Federal Reserve announced the resumption of quantitative easing (QE) in December, the central bank has expanded its balance sheet by over $200 billion.

During QE, the central bank buys U.S. Treasuries and/or mortgage-backed securities on the open market with money created out of thin air. This represents artificial demand for Treasuries, driving interest rates lower than they would otherwise be, enabling the federal government to borrow more at a lower interest rate than it could if the Fed didn’t have its big fat thumb on the market.

On the other side of the equation, QE is inherently inflationary. The Fed injects newly created money into the financial system as it purchases these assets. An increase in the money supply is, by definition, inflation.

Since the Federal Reserve is effectively turning U.S. government debt into cash, this process is sometimes referred to as debt monetization.

When the Fed announced it would end balance sheet reduction, effective December 1, at its October 2025 meeting, I wondered out loud if the central bankers were about to restart QE.

Sure enough, it did.

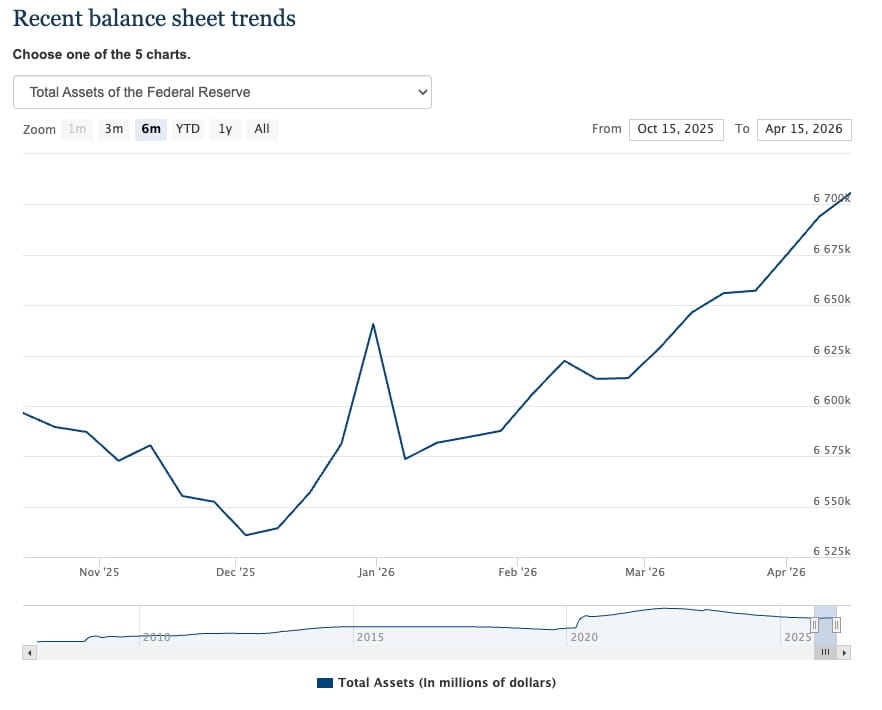

At the December meeting (Dec. 10), the FOMC announced plans to purchase $40 million in Treasury Bills that week (Bills are short-term Treasuries that mature in one year or less). From that point, the FOMC statement said, purchases will “remain elevated for a few months” before they are “significantly reduced.”

Nearly five months later, we’re still waiting for that “significant reduction.”

In the three weeks after the announcement, the Fed expanded the balance sheet by about $100 billion before drawing it back down in the first week of January. Since then, there has been a steady march higher, with the balance sheet now over $6.7 trillion.

Yes! This Is QE

Of course, you will not hear any central banker or mainstream pundit utter the words “quantitative easing.”

In fact, if pushed, they’ll almost certainly deny that they’re doing it. They’ll call it “reserve management,” or tell you they’re engaged in “technical operations” to keep the financial system’s plumbing moving.

However, an expansion of reserves is an expansion of reserves. You can call it QE. You can call it reserve management. You can call it tap dancing with unicorns.

In practice, the Fed plans to start buying Treasury bills with money created out of thin air. This will increase the money supply and put downward pressure on Treasury rates. The balance sheet will grow; liquidity will increase; risk asset bubbles will get more air. This is exactly what QE does. So, call it what you want. If it walks like a duck…

Why QE Now?

When Ben Bernanke launched the first round of quantitative easing during the Great Recession, he framed it as a temporary emergency measure. During a congressional hearing, he insisted that the Fed was not engaged in debt monetization, and when the crisis passed, the Fed would quickly shed the assets from its balance sheet.

That never happened.

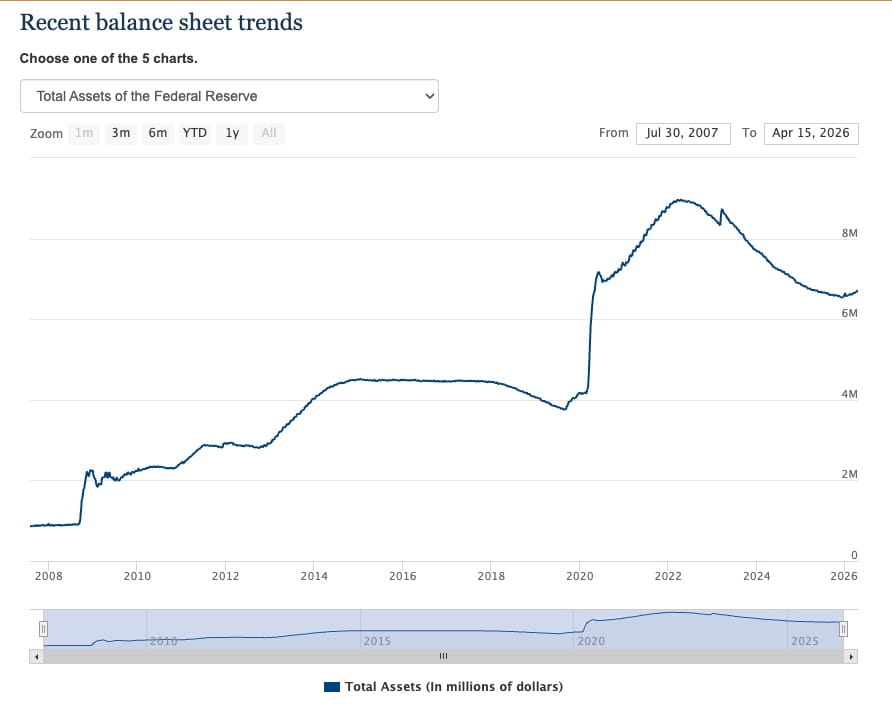

When the central bank started QE in late 2008, the balance sheet was around $900 billion. After three rounds of quantitative easing, the balance sheet had exploded to over $4.5 trillion.

The Fed made a half-hearted effort to shrink the balance sheet in 2017, but that economy got wobbly, and the stock market crashed in the fall of 2018. By 2019, the balance sheet was expanding again.

Of course, the balance sheet exploded again during the pandemic, reaching nearly $9 trillion by the time it was all said and done.

QE was conceived of as an emergency measure. So, what’s the emergency today?

The brief spell of QE in 2019 before the pandemic gives us a clue.

The Fed didn’t get around to tightening monetary policy until nearly a decade after the 2008 financial crisis. When it did, the economy threw a temper tantrum. That’s because the central bank hooked the economy on easy money. It incentivized massive levels of debt and blew up multiple asset bubbles. When the pusher tried to take the drug away, the addict went into withdrawal. Instead of letting the addict detox and sober up, the pusher supplied more drugs.

The pandemic gave the central bankers exactly the excuse they needed to inject a massive amount of liquidity into the system and prop up the floundering economy. I’m convinced that had the pandemic not come along, the economy would have tilted into a deep recession and possibly another financial crisis. That’s because an easy-money addicted economy can’t function in anything approaching a normal interest rate environment.

Fast forward to today.

The unprecedented scope and speed of pandemic-era money creation predictably led to price inflation. The Fed had no choice but to respond. It raised interest rates and shrank the balance sheet. But the economy is still addicted to easy money. It still can’t function in a normal interest rate environment.

And that, ladies and gentlemen, is why the Fed is running QE (while not calling it that) today.

It’s trying to walk a tightrope between taming price inflation with higher rates and avoiding the impact of a massive Debt Black Hole that demands lower interest rates.

This Catch-22 explains why we’re seeing balance sheet expansion despite price inflation still running above the stated 2 percent target. It is trying desperately to maintain the federal government’s ability to service relentless deficits while not triggering another unacceptable wave of price inflation.

Interestingly, the U.S. Treasury is also in on the act. It has bought back a record of $75.6 billion in Treasuries so far this year.

This debt buyback is a backdoor way for the government to suppress yields. It’s something of a Ponzi scheme. In practice, the Treasury issues new short-duration debt and uses proceeds to buy back longer-term debt. This shortens the average maturity of outstanding debt and puts downward pressure on the long end of the yield curve.

This strategy comes with its own set of risks. When the shorter-term debt comes due, it will have to be rolled over at the current interest rate. With yields generally rising, the new debt will likely carry a higher interest rate price tag than the maturing bonds. In essence, the Treasury is playing kick the can down the road, hoping the lower end of the yield curve doesn’t spike and that they can hold their overall interest expense down.

Keep in mind, the government is already paying more than $1 trillion per year just to service its massive debt. It has become the second-largest spending category for the federal government behind only Social Security.

The fact that the Fed is running QE (but not calling it that) reveals a dirty little secret. Political posturing aside, the central bank will pick inflation over allowing the economy to crash under the weight of its debt burden. One should plan accordingly.

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

in December, the central bank has expanded its balance sheet by over $200 billion.){kind=link}