(Money Metals News Service) Yesterday was Tax Day. It’s a source of misery for many of us as we write a big check to the IRS. But did you know the IRS isn’t the source of your biggest tax bill? In fact, you don’t even get a bill. You just pay the tax every time you buy something.

No, I’m not talking about the sales tax. I’m referring to the inflation tax.

Yes, ladies and gentlemen. Inflation is a tax.

When the government spends far more than it takes in, it has to borrow money. To support the borrowing, the Federal Reserve runs quantitative easing operations, buying Treasuries with money created out of thin air. This creates artificial demand for U.S. debt, suppressing interest rates and allowing the government to borrow more than it otherwise could.

You get goodies, and the government avoids raising taxes.

It’s a win-win, right?

Except you’re still paying taxes, you just don’t see it as clearly.

When the Fed creates money out of thin air and injects it into the economy, it drives price inflation.

The COVID Inflation Tax

Remember all those stimmy checks during the pandemic? Uncle Sam handed out some $930 billion in stimulus to individuals with three rounds of stimmy checks in 2020 and 2021. Meanwhile, the Federal Reserve expanded its balance sheet by nearly $5 trillion.

You’re still paying for that stimulus today.

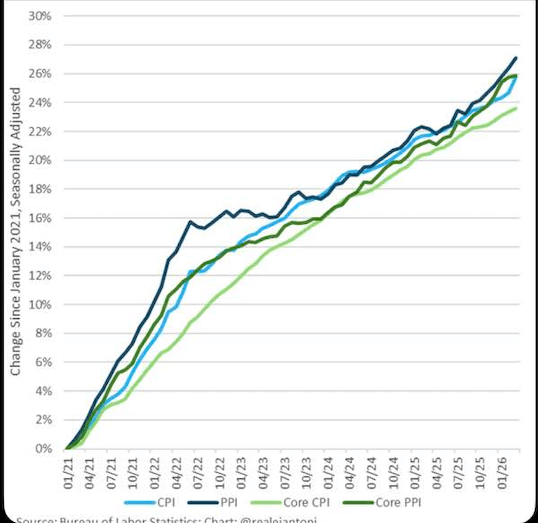

The thing about inflation is it’s cumulative. It creeps up gradually – a few tenths of a percent this month, a few tenths of a percent the next. It can almost seem like no big deal, but it adds up.

Since January 2021, price inflation is up between 23.6 percent and 27.1 percent, depending on which metric you choose to use.

To put it another way, the government has stolen around a quarter of your purchasing power in just five years.

It’s actually worse than that because every one of these metrics understates inflation.

The government revised the CPI formula in the 1990s so that it understated the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers. So, if the BLS used the old formula, we’d be looking at CPI closer to 50 percent. And using an honest formula, it would probably be worse than that.

The good news is your earnings are also impacted by inflation. The bad news is that wage inflation typically lags price inflation, so you are constantly playing catch-up. As consumers wait for their wages to catch up to prices, they’re forced to rely on savings and credit cards.

According to Federal Reserve data, average hourly earnings rose 24.9 percent in that same period. Based on the CPI data, even with that hefty raise, you’re just treading water. And when you consider that the CPI is understating price increases, you’re losing ground fast.

This underscores a couple of realities you should keep in mind.

- Nothing the government does for you is free. You and your children are going to pay – either through direct taxation or the inflation tax.

- Even in the best of times, you’re paying the inflation tax. Keep in mind that the government’s stated plan is to devalue your money by a little more than 10 percent every five years.

This is why it’s crucial to save in real money. As the inflation tax rises, so does the price of gold and silver. It protects your wealth from the insidious debasement that is part and parcel to this fiat system.

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

{kind=link}