(Mike Maharrey, Money Metals News Service) The shine has come off silver since it skyrocketed to over $100 an ounce in January. The price has dropped by over 50 percent from the record high. However, there are still reasons to be bullish on silver moving forward, including persistent supply deficits and growing industrial demand.

In a recent precious metals analysis, Sprott strategist and managing partner Paul Wong noted that silver recorded its largest monthly dip since September 2011 in June, capping off a quarter when silver fell by $16.57 per ounce, a 22 percent decline. It was the worst quarter since the first quarter of 2020, during COVID panic selling.

“Silver’s selling wave in June tracked gold’s plunge and was driven by the same macro forces: an expectedly hawkish Fed raising short-term rates and the U.S. dollar. Silver easily broke below support levels in a near-waterfall pattern, suggesting capitulation-driven selling sentiment.”

Wong noted that volatility isn’t unusual in the silver market.

“Silver has shown significantly greater volatility than gold due to its smaller and less liquid market. Sharp drawdowns are a normal feature of silver bull markets, not evidence that the underlying fundamentals have failed. Historically, some of silver’s strongest advances have occurred following periods of severe volatility and investor frustration.”

With this in mind, Wong thinks silver remains in a “strong positive position” from both a fundamental and technical standpoint.

“Despite the recent wrenching volatility, over a multi-decade period, the silver chart remains among the most bullish chart patterns we are aware of.”

Wong categorized silver as “one of the most volatile parts of the precious metals complex,” noting that the sharp correction and wild price movements have “tested sentiment.”

“But silver’s long-term bullish fundamentals appear unchanged. These rest on the combination of constrained supply and growing demand.”

Not Enough Metal

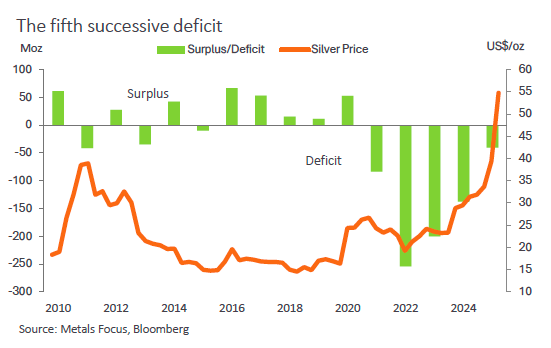

Silver has been in a structural market deficit for five years, meaning demand for the metal has outstripped mining and recycling output. Last year, demand outstripped supply by 40.2 million ounces (1,250.36 tonnes). That drove the 5-year market deficit to 716 million ounces. To put that into perspective, total silver mining output last year was 846 million ounces.

Metals Focus expects the supply shortfalls to continue, with a projected 46.3-million-ounce supply deficit this year.

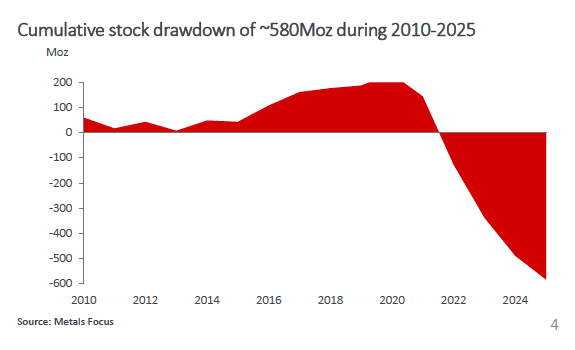

Before this string of successive market deficits, there was a cumulative above-ground stock rise of 243 million ounces between 2010 and 2020. Taken together, there has been a stock rundown of around 473 million ounces in the last 15 years.

This shortage of metal was the root cause of two silver squeezes. The first drove silver to over $50, and the second took it to well over $100.

When silver demand outstrips mining and recycling output, silver users must tap into aboveground stocks. That generally means rising prices to incentivize those holding silver to give it up.

As Metals Focus explained, that’s exactly what happened last fall.

“Against this backdrop, shifts in inventories into CME vaults, rising ETP holdings, and a spike in physical demand created an unprecedented liquidity squeeze in October.”

Tariff worries drove a flood of metal from London to New York in the spring of 2025. When silver demand spiked last fall, there wasn’t enough metal in London vaults to meet the sudden offtake. While the movement of metal back to London eased the immediate strain, it didn’t solve the fundamental problem – not enough physical metal.

As Wong explained, silver supply is relatively inelastic, meaning it doesn’t respond quickly to rising prices.

“Unlike many commodities, there are few large new mining projects that could materially alter the medium-term supply outlook. Silver supply is relatively inelastic even as demand continues to expand.”

Meanwhile, the growing solar industry and the AI buildout continue to increase industrial demand for silver.

“Several secular growth trends support demand. Solar panel manufacturing, electrification, electric vehicles, AI infrastructure, data centers and a wide range of technology applications underpin industrial demand for silver. Military consumption is also becoming increasingly important as silver’s conductivity and strategic importance gain recognition across defense supply chains. Even in a slower economic environment, many of these end markets are likely to remain supportive.”

The higher price has increased silver investment demand.

“Investors often focus on gold as the primary monetary metal, but silver has historically participated in periods of currency debasement and monetary uncertainty. In this environment, silver benefits due to its growing appeal as an alternative store of value, essentially a higher-beta expression of the same themes that support the gold market.”

Wong said he wouldn’t be surprised if deficits continue for the next seven or eight years.

Wong also noted the outsized impact of paper silver on the market. He pointed out that massive bets in the options markets helped drive prices to record highs. Wong said call options outstanding and open interest reached four or five standard deviations above their norm during the price spike.

“Until you get rid of all these crazy options positions, it’s more of a meme stock than a commodity in the short term. But eventually what happens is you’ll shake out the option guys.”

Over the last several months, the call options have generally returned to the mean, and the unwinding of those positions has magnified the price decline.

Despite the impact of paper trading, Wong said the physical market will ultimately win the day.

“Tightness in physical inventories and ongoing delivery pressures have reinforced the view that physical demand remains strong relative to available supply,” he wrote. “As more metal flows toward Asian markets and physical ownership continues to gain importance, paper-market pricing mechanisms may become less influential over time.”

Given these dynamics, Wong said he thinks silver’s long-term price outlook remains “positive.”

“Silver’s unique combination of persistent supply deficits, expanding industrial demand, increasing monetary relevance, and tight physical market conditions provides multiple avenues for future appreciation.”

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

{kind=link}