(Mike Maharrey, Money Metals News Service) Silver has been on a wild roller coaster ride.

Is the recent selloff a temporary correction or have we reached the end of the rally?

While the supply displacement that pushed silver to a new record high has moderated somewhat, the underlying dynamics that have been driving both silver and gold higher over the last two years remain in place.

Silver gained nearly 40 percent in two months. This is the definition of overbought, and a correction was inevitable.

Correct it did.

After charting a new record high of $54.48 in mid-October, silver suffered the largest single-day selloff in years just 11 days later, plunging 16 percent to a low of $45.57 on October 28. Since then, silver seems to have found support in the $48 range.

It’s important to remember that even with the sharp correction, silver is still up over 65 percent this year and ranks among the best-performing assets.

Silver’s selloff corresponded with a similar correction in the gold market. Metals Focus called the correction “long overdue.”

“Following an exceptional rally since late August, all technical indicators suggest that both silver and gold had entered overbought territory. Given growing concerns over the sustainability of the rally, some technical profit-taking was to be expected.”

The Silver Squeeze

One of the factors that pushed silver higher so quickly was a silver squeeze.

A convergence of factors from market dynamics to logistical problems led to this unprecedented silver shortage in London. While the market dynamics that got us here might be difficult to untangle, the situation is about as basic as it gets.

There’s not enough silver.

The movement of silver to New York earlier this year, as tariff worries intensified, depleted London vaults. Meanwhile, silver demand in India surged, putting more pressure on the London market.

According to Bloomberg, the amount of free float silver available in London dropped from a high of 850 million ounces to just 200 million ounces, a 75 percent decline. Metals Focus estimates that the available metal fell closer to 150 million ounces.

According to Metals Focus, supply displacement has moderated.

After peaking at just over 530 million ounces at the end of September, silver holdings in COMEX-approved vaults have declined by more than 44 million ounces, putting October on track for the largest monthly outflows on record. According to Metals Focus, “A substantial portion of these outflows is believed to have been redirected to London.”

Meanwhile, silver demand in India cooled as the Diwali festival came and went. This is evidenced by a sharp decrease in local premiums.

Additionally, profit-taking in silver ETFs freed up some metal, easing the physical tightness in the market.

These factors combined have helped ease the market pressure, at least for the time being. But the entire drama signals more structural problems in the silver market.

Fundamental Supply Issues

The root of the problem is simple: there isn’t enough metal to meet demand. And there is way too much paper silver floating around without any metal backing it. While shuffling silver between London, New York, and India took the immediate pressure off the market, it didn’t magically create new silver.

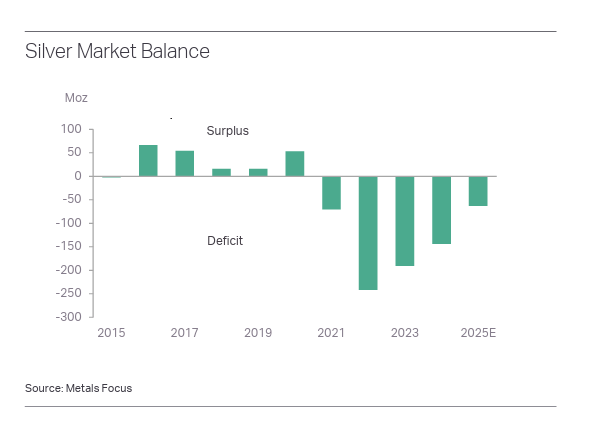

Silver demand has outstripped supply for four straight years. The structural market deficit came in at 148.9 million ounces last year. That drove the four-year market shortfall to 678 million ounces, the equivalent of 10 months of mining supply in 2024.

The Silver Institute projects a fifth straight supply deficit this year.

Industrial demand has been at record levels for the last two years. Now we’ve added significant investment demand to the equation. We will likely see more supply squeezes in the future.

Part of the problem is that silver mines can’t keep up with demand, and mine output has generally sagged since peaking in 2016.

Metals Focus forecasts that while we will see record silver prices over the next five years, “mine supply growth is likely to remain modest, with only minimal increases globally.”

Why won’t silver production ramp up to meet the demand and take advantage of these higher prices?

Metals Focus blames the price inelasticity on the fact that more than half of silver is mined as a byproduct of base metal operations.

“Although silver can be a significant revenue stream, the economics and production plans of these mines are primarily driven by the markets for copper, lead and zinc. Consequently, even significant increases in silver prices are unlikely to influence production plans that are dependent on other metals.”

About 28 percent of the silver supply is derived from primary silver mines, where production is more tightly tied to price. But silver mines face their own challenges, including declining ore grades and rapidly rising mining costs.

The bottom line is we can’t expect a sudden surge in mine production to solve this fundamental supply problem.

As Metals Focus summarized it:

“A continued deficit in the silver market, coupled with refining capacity bottlenecks for silver scrap, will also help keep physical supply relatively tight. This leaves the market vulnerable to further liquidity squeezes.”

Other Bullish Dynamics in the Silver Market

According to Metals Focus, “The factors that have driven significant investment inflows into the precious metals complex are expected to remain intact well into 2026.”

These factors include the likelihood of a lower interest rate environment. Despite persistently sticky price inflation, the Fed seems intent on easing monetary policy. It cut rates by another quarter-percent at the October meeting and announced it will end balance sheet reduction.

Metals Focus pointed out that even if the Fed ends up easing less aggressively than anticipated, the lower real interest rate environment will still reduce the opportunity cost inherent in holding precious metals.

“During this period of declining interest rates, tariff-induced inflation may initially strengthen before easing, potentially leading to a more rapid decline in real interest rates.”

According to Metals Focus, growing concerns about global government debt will also support silver in the longer term. The U.S. national debt recently eclipsed $38 trillion. The fact that nobody seems inclined to address the U.S. government’s borrowing and spending problem continues to undermine faith in the dollar.

“Questions surrounding the long-term viability of the U.S. dollar as the dominant reserve currency, and ongoing geopolitical tensions, are all likely to support silver, albeit indirectly, through its close relationship with gold.”

We can expect continued volatility in the silver market in the coming weeks, but given the underlying fundamentals, it seems unlikely that the bull market has run its course, and price drops could be viewed as buying opportunities.

{kind=link}