(Mike Maharrey, Money Metals News Service) Platinum group metal prices rose substantially last year, driven by persistent supply deficits and favorable market dynamics, and Metals Focus expects the bull market to continue this year, with significant price upside remaining.

Platinum joined gold and silver for the wild ride up in 2025, gaining 119 percent, and then continuing to surge through the first three weeks of 2026. Platinum hit an all-time high of $2,923 an ounce in late January before selling off along with gold and silver.

Palladium took a similar trajectory, rising 78.7 percent in 2025 from $914.10 before peaking just below $1,100 in January.

According to Metals Focus, several factors drove PGM prices higher, including tightening physical balances, increasing investor interest, and concerns about the possible impact of trade and strategic access policies on trade flows.

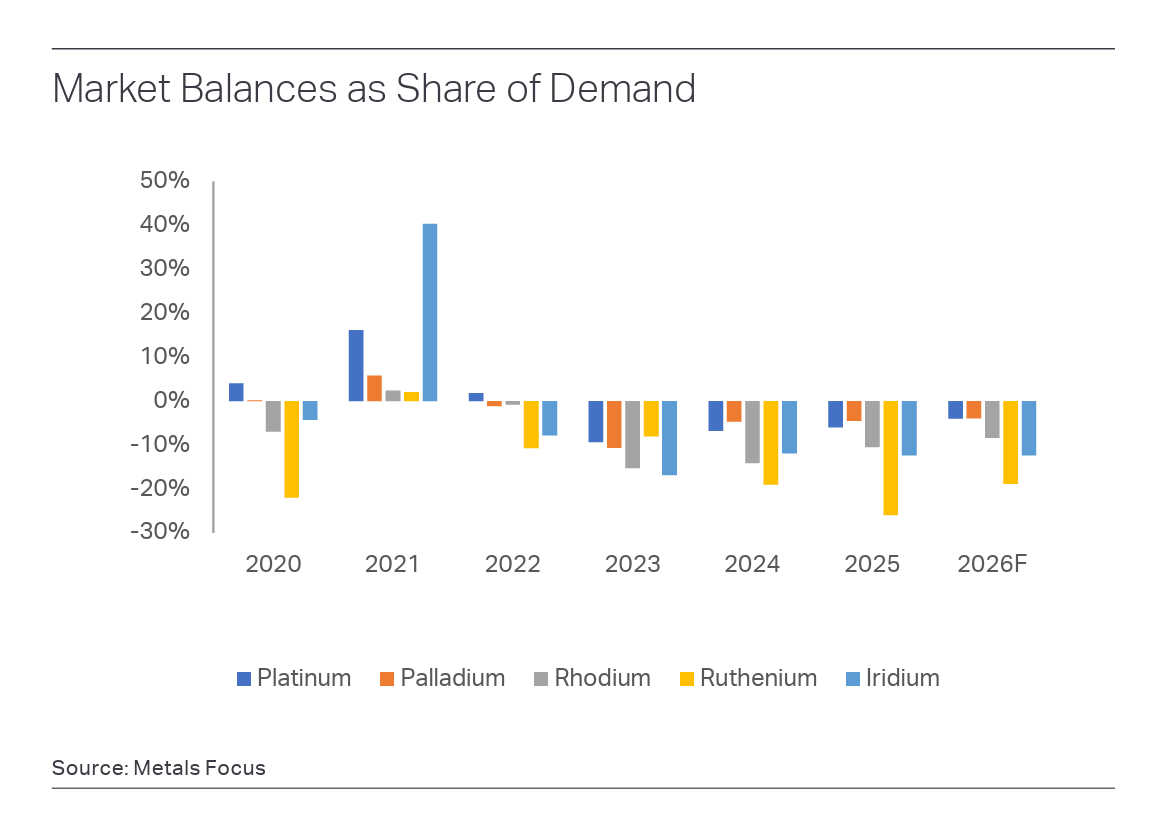

Persistent market deficits have squeezed both the platinum and palladium markets. In 2025, platinum demand outstripped supply by 951,000 ounces. It was the fourth straight market deficit, with the supply shortfall widening significantly from 559,000 ounces in 2024.

The palladium market deficit nearly doubled from 218,000 ounces in 2024 to 416,000 ounces last year.

This is similar to what happened in the silver market, where persistent deficits finally reached a critical mass and drove two squeezes that sent prices sharply higher. When production dips below demand, users must source metal from existing above-ground stocks. This generally requires higher prices to incentivize sellers.

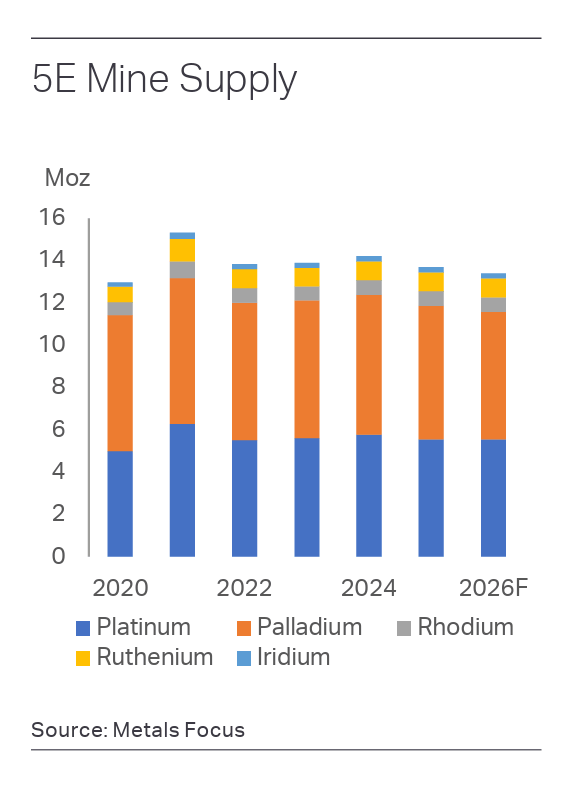

Declining mine output is squeezing the platinum supply.

Total platinum mine supply fell by 4 percent to 5.6 million ounces last year. Palladium mine output mirrored the percentage decline, contracting to 6.3 million ounces.

Secondary supply provided a partial offset, with total PGM scrap rising.

According to Metals Focus, several factors impacted PGM mine output, including a disruption in South African production due to flooding at several operations and a sharp decline in North American supply following the placement of Stillwater West on care and maintenance.

On the demand side, automotive offtake for PGMs (platinum, palladium, and rhodium) fell modestly by 2 percent to 11.9 million ounces in 2025. Notably, it was the first time auto demand dipped below 12 million ounces since a chip shortage impacted the industry in 2022.

According to Metals Focus, light-duty vehicle production grew 3 percent last year, but gains were skewed towards battery electric vehicles (BEV), which achieved a 16 percent market share.

“The pace of electrification will remain the central question for these three key PGMs. In 2025, ICE and hybrid production still accounted for the vast majority of light vehicles, but BEVs penetration is increasing steadily.”

Increasing demand in other sectors, particularly investment offtake, took up the slack.

“What has changed markedly is the investor story. Platinum’s re-rating last year was driven as much by strategic accumulation and correlation with gold as by physical fundamentals and tighter available stock levels, and that dynamic alongside the risk of protracted U.S.-Iran conflict will likely continue to shape pricing in 2026.”

Retail investment demand surged by 96 percent to 404,000 ounces. Record Chinese buying accounted for roughly 60 percent of global purchases.

PGM offtake for other industrial applications also rose last year.

Electronics demand rose by 8 percent to 1.3 million ounces across all PGMs, thanks to the AI boom.

Chemical demand grew 3 percent to 1.9 million ounces. Palladium is an important input in plastic precursor production.

Meanwhile, platinum jewelry demand rose 10 percent to a 9-year high of 2.2 million ounces. Surging platinum jewelry sales continued the upward trend that began in 2024, with manufacturers pivoting to platinum as gold prices surged.

Metals Focus expects the PGM market deficits to continue in 2026. However, “price outcomes will increasingly be shaped by investor flows, stock movements and policy intervention rather than supply-demand balances alone.”

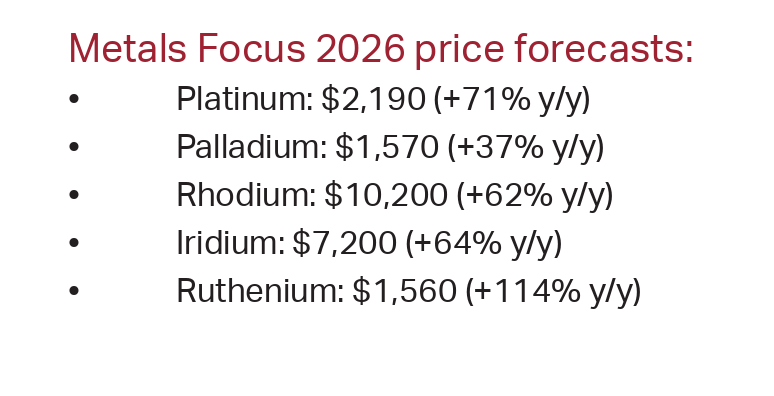

“Platinum is forecast to remain in a fourth consecutive deficit of 312,000 ounces, with above-ground stocks declining to 9.0 million ounces. Following a sharp re-rating in 2025, driven by the launch of platinum futures on China’s Guangzhou Futures Exchange (GFEX) and other investment inflows, the metal is expected to consolidate at elevated levels, averaging $2,190 in 2026 (+71% y/y). Palladium, while still in deficit for a fifth consecutive year at 376,000 ounces, faces limited investor appetite, keeping it at a discount to platinum, with a forecast average of $1,570 (+37% y/y).”

Based on its market analysis, Metals Focus expects the price of all the PGMs to rise further in 2026.

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

{kind=link}