(Money Metals News Service) Retail bargain hunters stepped in significantly over the past few days as gold and silver markets suffered their sharpest setback in several months last week.

The selloff was driven less by any deterioration in precious metals fundamentals and more by a rapid repricing of interest-rate expectations following stronger-than-anticipated U.S. economic data.

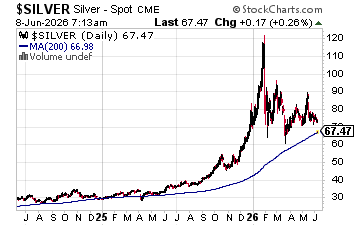

Silver is testing its 200-day moving average, a key price support level.

Gold declined nearly 5% for the week, while silver plunged almost 9%, extending a correction that has gathered momentum since reaching multi-month highs earlier this quarter. Silver once again demonstrated its more volatile nature, amplifying gold’s downside move and causing the gold-to-silver ratio to widen significantly.

The primary catalyst was the May U.S. employment report. Non-farm payrolls increased by 139,000 jobs, surpassing expectations, while the unemployment rate held steady at 4.2%. The data reinforced the perception that the labor market remains resilient despite mounting concerns over slowing economic growth, which reduced expectations for near-term Federal Reserve rate cuts.

That shift pushed Treasury yields and real interest rates higher while boosting the U.S. dollar. Since precious metals compete with interest-bearing assets for investor capital, rising real yields tend to create headwinds for both gold and silver.

The payrolls report effectively removed a portion of the safe-haven premium that had accumulated in recent weeks and triggered widespread liquidation among leveraged futures traders.

Geopolitical risks offered little support. Ongoing hostilities in the Middle East and elevated energy prices failed to generate meaningful safe-haven buying. Instead, investors focused on the inflationary implications of higher oil prices and the possibility that sticky inflation could force the Federal Reserve to keep policy restrictive for longer.

From a technical perspective, the damage was significant. Gold broke below both its 20-week and 40-week moving averages while momentum indicators deteriorated.

Silver’s chart also weakened substantially, although the metal remains near important longer-term support levels and has not yet confirmed the same degree of structural breakdown seen in gold.

Despite the sharp decline in paper markets, physical demand remains relatively healthy.

Buyers in North America and Asia have stepped in to take advantage of lower prices.

Meanwhile, silver continues to benefit from strong long-term industrial demand tied to electrification, solar installations, grid upgrades, and data-center expansion.

Premiums on coins, bars, and rounds remain at the lowest point seen since last year.

{kind=link}